The SCFI retreated by 4.3% last week after a 10-week run of successive rate hikes as new capacity additions relieved some of the vessel space tightness that has driven spot rate gains of over 70% since April. Carriers failed to hold on to the early July rate hikes as rates receded across the board. Although carriers are still pushing for 2 more rounds of rate hikes on 15 July and 1 August, rates appears to have peaked for now with space constraints starting to ease with new deliveries and capacity evacuated from the Persian Gulf easing some of the market tightness. Total capacity still idle within the Gulf is down to only 30,000 teu from a peak of 490,000 teu with only limited inbound traffic through the Strait of Hormuz. Of the few non-Iranian ships that has risked entering the Gulf, the 6,969 teu GFS GALAXY has been incapacitated after a missile attack on its outbound voyage from UAE on 12 July that has triggered the US to declare an end to the ceasefire in Iran.

Severe weather across China last week resulted in a large backlog of vessels waiting to berth with over 2m TEU of vessel capacity currently waiting in North Asia mostly around Shanghai and Ningbo which will take several weeks to clear.

Johnson Leung

Johnson Leung

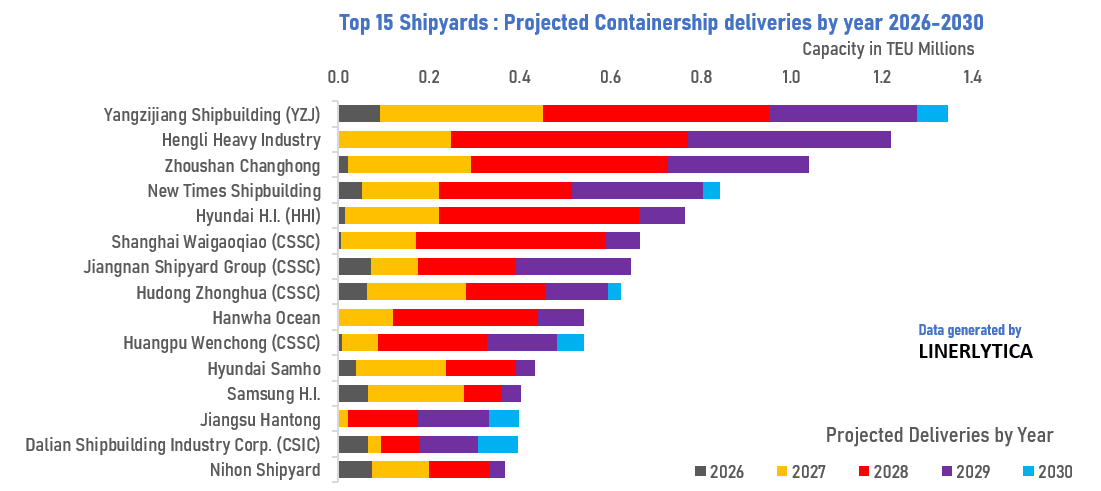

Chinese shipyards dominant as containership orderbook hits new high

The containership orderbook has passed 40% of the current fleet as it hits a new high of 1,712 ships for 13.72m TEU. Chinese shipyards account for 8 out of every 10 ships on order with 10 of the top 15 yards located in China. The top 4 yards currently are all privately-owned Chinese shipbuilders, with the notable emergence of Hengli Shipbuilding which only started in 2022 when it took over the facilities of the bankrupt STX Dalian shipyard. Hengli has grown to become the 2nd largest builder of containerships and is poised to challenge compatriot Yangzijiang Shipbuilding for the top spot as it continues to add to its expanding orderbook with 56 containerships secured in the first 6 months of this year alone.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year