The vessel evacuations from the Persian Gulf continue despite Iranian threats as 26 containerships with a total capacity of 195,000 teu or more than half of the stranded ships have already withdrawn from the Gulf. Activity within the Gulf has also picked up with over 60 ships now employed on intra-Gulf services as the idle fleet dropped by more than 40 units over the past 2 weeks.

Strong cargo demand across all tradelanes have pushed global TEU-mile demand growth to 7.3%, while vessel supply growth remains constrained at 5.4%, as the demand-supply gap widens to its highest level since December 2024. Port congestion has also worsened to their highest levels since 2022 with 10.9% of the fleet currently waiting at anchorages. All of these factors have helped to push up both freight and charter rates as the SCFI breached 3,200 points with the positive momentum expected to last for at least another month. EC freight futures point to a July rate peak as carriers push ahead with a fresh round of rate increases on 1 July given the current tight market conditions.

Johnson Leung

Johnson Leung

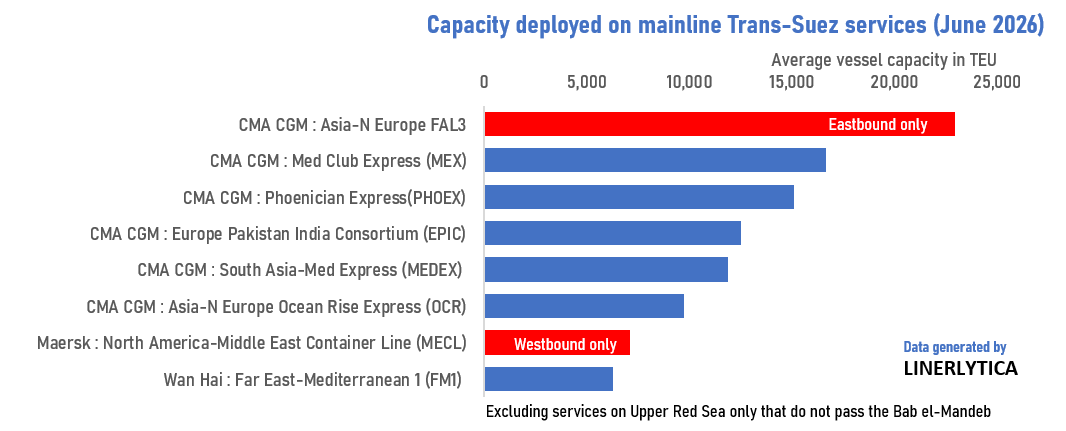

Maersk continues to eye an early return to trans-Suez route

Maersk has resumed Suez transits on its Middle East Container Line (MECL) service with 3 westbound sailings since 13 June, after abandoning an earlier plan first announced on 15 January 2026 due to the Iran war. CMA CGM has also mounted 5 eastbound trans-Suez sailings on the FE-Europe FAL3 service in June, in addition to 5 other services that it already operates on the Suez route on both directions. Wan Hai is the only other mainline carrier on the regular Suez route, excluding smaller niche carriers serving the Baltic Russia and Black Sea/Turkey routes.

According to Linerlytica’s data, there are over 780 ships deployed across 60 services that are still diverted from the Suez to the Cape route currently with a total capacity of 11.3m TEU. If all of these services return to the Suez route, it would release more than 120 ships for 1.7m teu which account for 5% of global fleet capacity.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year