The re-opening of the Strait of Hormuz after the US-Iran peace deal due to be signed this Friday will release some 51 containerships with a total capacity of 300,000 teu presently stranded in the Persian Gulf (full list of ships in page 2). The capacity set to be evacuated from the Gulf could provide some short-term relief to an over-stretched container market but uncertainty remains over when regular services to the Persian Gulf can be restarted which would add to additional vessel demand.

Freight rates continue to surge across the board as the mid-June rate hikes will push this week’s SCFI assessments even higher, with the increased rates set to persist through the end of July on high peak season demand that has been additionally boosted by US tariff relief as well as the AI and green energy cargo boom. With containerships in short supply and charter rates remaining elevated, some carriers may be tempted to resume Red Sea transits, with Maersk already deploying 2 of their ships back to the Bab el-Mandeb in the past 2 weeks.

Johnson Leung

Johnson Leung

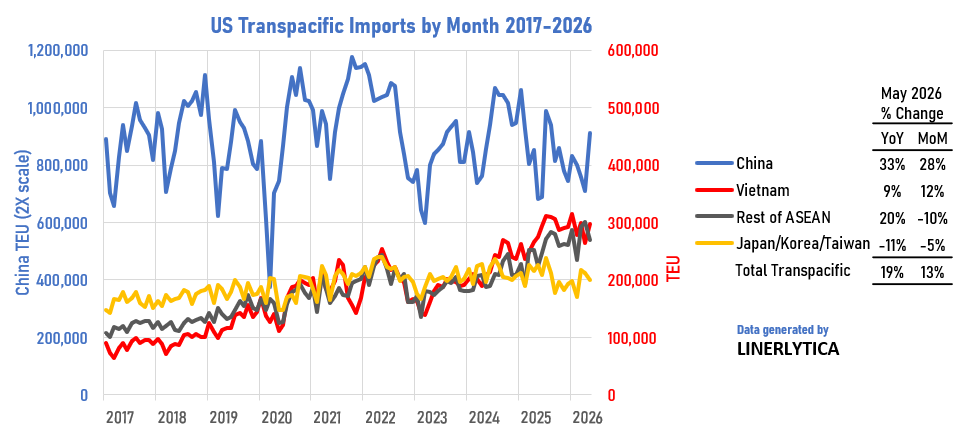

Chinese exports to US rebound on IEEPA tariff relief as well as AI and green energy boom

Transpacific container volumes rebounded strongly in May 2026, driving a sharp rise in freight rates on surging capacity utilization. Total container arrivals from the Far East increased by 19% YoY and was also up 13% MoM with exports from China recording the largest gains at 33% YoY and 28% MoM, outperforming all other Transpacific origins including Vietnam and the rest of Southeast Asia. The reduction in effective tariffs on Chinese goods under current Section 122 that replaced the IEEPA tariffs since the end of February and a dramatic boom in AI-related technology goods and renewable energy products have contributed to the cargo rebound. Transpacific freight rates to the US West Coast have surged past $6,000/feu from $1,800/feu in February with the higher rates set to last to July backed by the increased cargo demand.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year