The SCFI index rose sharply by 15.9% to reach 2,572 points, and has risen by 92.9% since the Iran-US conflict started 3 months ago. The prolonged Hormuz blockade and high oil prices have not dampened cargo demand, but have instead spurred further growth of clean energy goods while US imports have been boosted by the removal of the IEEPA tariffs. The strong container freight rate momentum looks set to last at least until the end of July as carriers continue to cash in on the high peak season demand to push another series of rate hikes in mid-June following the successful 1 June rate increase and peak season surcharge application with the freight futures markets pricing in a July market peak.

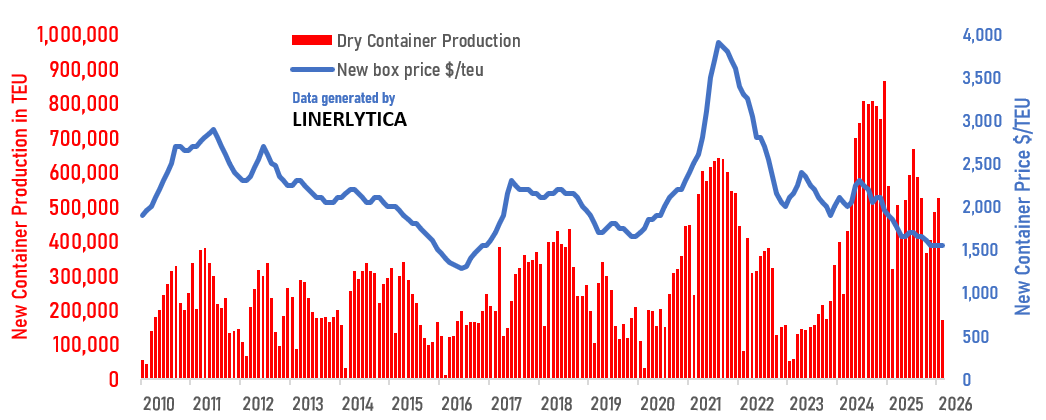

Despite the increased demand, container equipment availability remains adequate with over 1.2m TEU of new box inventory in China, compared to a peak of 1.8m TEU last year. New container production reached a record high in 2024 at over 186% above the pre-COVID annual average despite US DoJ allegations of a conspiracy to restrict production by the 6 largest container manufacturers in China.

Johnson Leung

Johnson Leung

New container production reached record highs in 2021 and 2024

The US Department of Justice has accused 6 Chinese container manufacturers of restricting the production of new containers and fixing the prices of dry containers during the period from November 2019 through January 2024. Based on court documents publicly released on 19 May, it is alleged that prices of dry freight containers doubled between 2019 and 2021 as a result of the conspiracy between CIMC, CXIC, Dong Fang, Singamas and 2 more Chinese container manufacturers that together account for over 95% of new box production globally. According to Linerlytica’s analysis of a box production over the last 25 years, the sharp increase in new container prices in 2021 was due to the surge in demand during the COVID pandemic, with the 6 manufacturers ramping up production correspondingly as the total new dry freight containers produced in 2021 reached a record high of 6.61m TEU and was surpassed again in 2024 when 7.85m TEU of new boxes were added as demand surged following the Red Sea diversions.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year