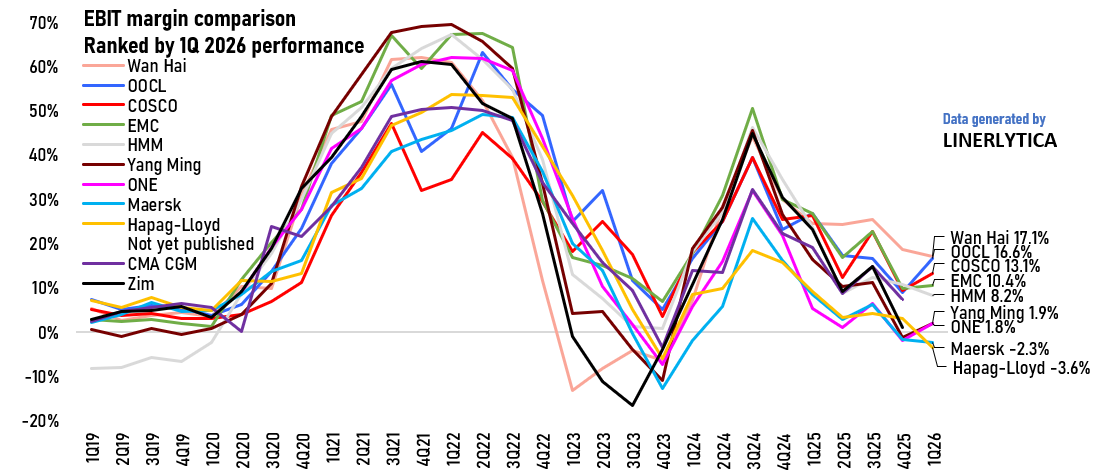

A year after the launch of the Gemini Cooperation by Hapag-Lloyd and Maersk, the 2 partners continue to under-perform the rest of the market as earnings plunged and turned negative in the 1st quarter despite the purported cost savings from the Gemini alliance. Continued losses are expected for the rest of this year even though all of their main rivals have posted positive earnings after freight rates rebounded in the 1st quarter.

The rate momentum remains positive, with TEU-mile demand growth moving ahead of supply growth allowing carriers to push ahead with their mid-May rate hikes. The early peak season rush has raised capacity utilization and carriers are pushing for another round of rate hikes and peak season surcharges to be applied from 1 June. Vessel demand remains very high with additional peak season loaders due to be launched in June centred around the Transpacific and Indian subcontinent even as the Hormuz deadlock remains unresolved with traffic still closed, although several Iranian linked ships were still able to transit last week.

Johnson Leung

Johnson Leung

Profits remain elusive for Gemini partners

Hapag-Lloyd and Maersk remain firmly planted at the bottom of the carriers’ earnings league table, with both carriers reporting negative EBIT earnings in the first quarter of 2026 while their main rivals have all posted positive earnings. The 2 Gemini Cooperation partners continue to eye an early return to the Suez route as they are running out of solutions for their persistently poor results. Although Hapag-Lloyd blamed adverse weather in the North Atlantic and the Middle East conflict for its poor performance, the larger problem lies with their high dependency on contract customers and the Gemini Cooperation’s emphasis on schedule reliability that has failed to translate into higher freight rates while placing rigid constraints on their ability to manage capacity through the use of blanked sailings.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year