Carriers’ have reversed the earnings slump in the 1st quarter with early financial results from COSCO and ONE showing EBIT margin improvements of some 4% compared to 4Q 2025. Freight rates have held up in the 2nd quarter, with carriers able to recover most of the fuel cost increases since March and persisting with regular bi-monthly rate hike announcements as they continue to test the resilience of cargo demand. Charter rates have also strengthened with vessel demand undiminished by the Persian Gulf crisis, and carriers remain locked in the incessant fight for market share. COSCO has added 12 more newbuildings, on top of new long term charter commitments for 16 more newbuildings from Costamare announced last week, but they are far from being the only carrier eyeing further fleet expansion as the orderbook has swelled to a new record high of 13m TEU on the back of unrestrained new ship orders.

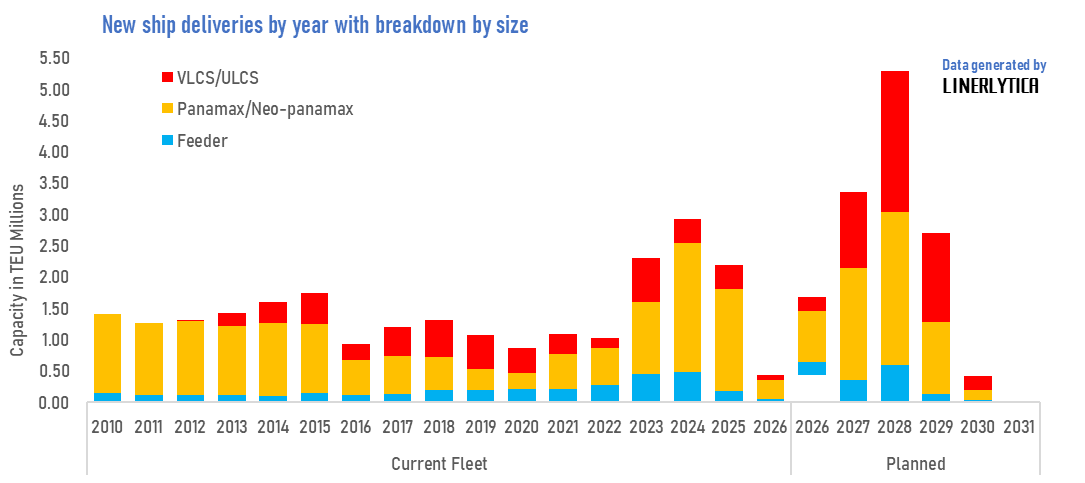

Over-capacity will soon catch up with the market with over 5m TEU scheduled to be delivered in 2028 alone.

Johnson Leung

Johnson Leung

Bloated 2028 new containership delivery backlog still growing

The containership orderbook has reached a record high of 13m TEU following the recent spate of fresh newbuilding orders, pushing the orderbook ratio to a post-GFC high of 38.3%. Total new ship orders in the first 4 months of 2026 has already exceeded 1.9m TEU and is on track to beat the 2025 full year record high of 5.1m TEU of new orders contracted in a single year.

The bulk of the new deliveries are scheduled in 2028 where firmed orders have already reached 5.2m TEU, with a limited number of delivery slots still open. When fully filled, total deliveries in 2028 are expected to exceed 5.5m TEU.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year