The US Supreme Court ruling on IEEPA import tariffs lifted market sentiments but the impact on Transpacific market demand is likely to be muted as the new 15% global tariff announced by President Trump as well as the threat of further supplementary tariffs will largely neutralize the impact of the IEEPA ruling. The tariff uncertainty provides little incentives for shippers to alter their shipment plans to take advantage of the marginal reduction in the tariff rate in the short term. Transpacific arriers are nonetheless aiming to capitalize on any potential increase in volumes as they push ahead with the 1 March GRI with rates expected to rise by some $1,000 in the coming week, aided in part by the high number of blanked sailings that will remove more than 30% of the capacity over the 2 week post Chinese New Year holiday window.

Zim’s sale to Hapag-Lloyd will still need to clear Israeli political hurdles, as sceptical shareholders are still disposing Zim shares at a 20% discount to the offer price even as a rival Maersk bid was revealed. Maersk remains ambivalent on its next move after resuming Suez transits on the MECL and ME11 services despite rising US-Iran tensions.

Johnson Leung

Johnson Leung

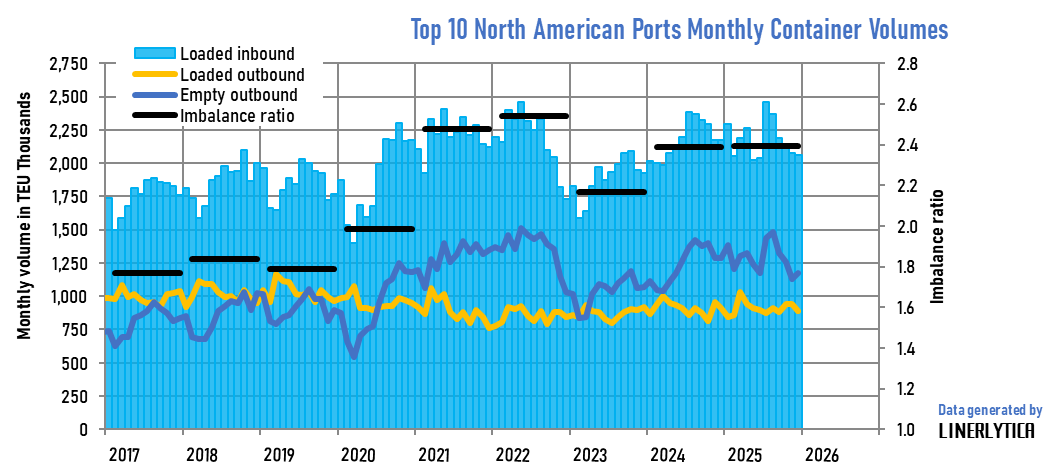

US container trade imbalance worsens despite Trump tariffs

The US container trade deficit continued to widen in 2025 despite the Trump tariffs with laden exports falling by -0.2% while imports grew marginally by 0.1%. Outbound empty container moves increased by 3.5% to 10.9m TEU at the 10 largest North American ports as the US container imbalance ratio remains at a post-pandemic high of 2.4 times. Early estimates of January volumes show declines in both container imports and exports with the removal of the IEEPA tariffs by the US Supreme Court expected to do little to reverse the imbalance in the absence of a coherent trade policy.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year