Hapag-Lloyd has agreed to pay $4.2Bn to acquire ZIM in the largest carrier consolidation move since 2017 when COSCO acquired OOCL. The deal will still require regulatory approvals and triggered a protest strike at Zim’s head office in Israel over the weekend. It comes as carriers’ ability to halt the rate slump will be tested again via another GRI push planned on 1 March despite the weaker cargo demand after the Chinese New Year holidays. The transpacific route is most at risk as carriers are inexplicably adding more transpacific capacity this year despite the weakening demand, setting the stage for a potential rate war. In contrast, Transatlantic capacity will be cut in response to the lower demand.

Maersk has made another U-turn as it diverts the first vessel scheduled to make the eastbound Suez transit on the MECL back to the Cape route last week, putting their plans to return to the Suez in doubt. Adverse weather conditions at the Bay of Biscay last week continues to disrupt ship schedules in and out of Europe, but it fails to explain Maersk’s U-turn as the ship was already in Mediterannean waters before it was redirected to turn south to take the longer Cape route.

Johnson Leung

Johnson Leung

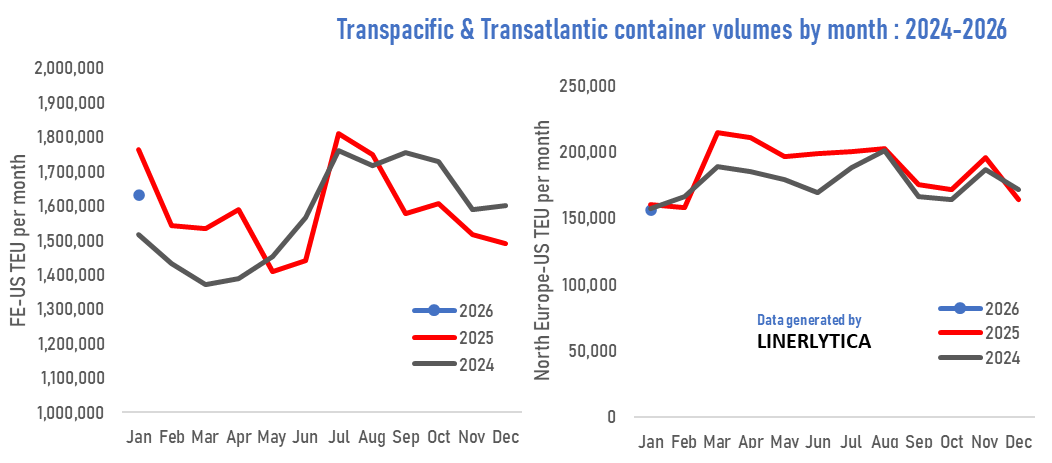

Weaker Transpacific volumes expected in 2026

Total Far East to US container volumes fell by 7.5% in January with cargo demand muted by the impact of US tariffs, coupled with the effects of front-loading last year that lifted volumes in the first quarter of 2025. Overall volumes are expected to remain muted for the remainder of 2026, especially around the key peak season window that stretches from June to September. Despite the cautious outlook, carriers will still be adding transpacific capacity led by the Premier Alliance and Wan Hai that will launch 2 new Far East to US West Coast services in April and May that will add some 12,000 teu per week on the route this year.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year