Carriers earnings are back in the spotlight after ONE posted an operating loss in the 4th quarter of 2025. Freight rates have continued to slip ahead of the Chinese New Year holidays and the carriers’ ability to stop the rate slump will continue to be tested in the coming months. Although global TEU-mile demand remains resilient and currently stants at 6.5% above last year’s levels, there are doubts over the sustainability of current cargo growth outside of the US as well as the continuation of vessel diversions away from the Red Sea and elevated port congestion.

Severe weather conditions in the North Atlantic last week pushed global congestion to a post-pandemic high as the total capacity tied up at anchorages briefly exceeded 10% of the global fleet. New ship deliveries dropped to a 35-month low of just 84,850 teu in January, against a monthly average of 206,000 teu in the last 3 years. But the pace of deliveries will soon start to pick up again with the orderbook rising to a post-2010 high of 36% as new orders continue to be added at a frenetic pace with 550,000 teu contracted in January alone.

Johnson Leung

Johnson Leung

Liner shipping cash windfall set to end

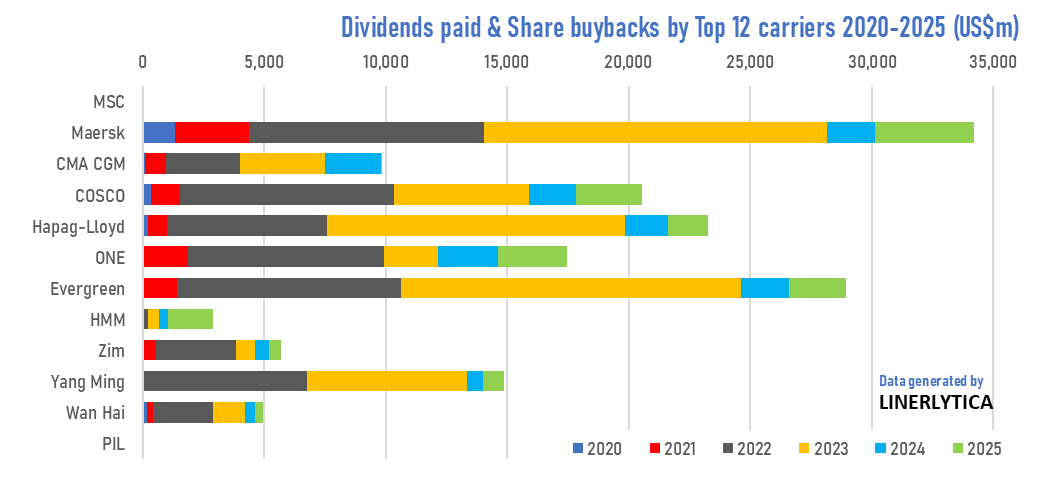

10 of the top 12 carriers have paid back over $160 Bn to their shareholders since 2020 through outsized dividend payments and share buybacks but the cash windfall would soon dry up as the container shipping super-cycle comes to an end. ONE reported an operating loss of $84m and net loss of $88m in the 4th quarter of 2025, with Maersk and Hapag-Lloyd also expected to report negative operating profit figures for their liner shipping business units when their results are announced later this week.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year