Trump’s Greenland tariffs would threaten the fragile balance on the Transatlantic container trades, with westbound rates from Europe to the US already down by 40% since the beginning of 2025. But carriers face a bigger challenge away from the Transatlantic arena as freight rates out of Asia are eroding despite earlier expectations of a market rally ahead of the Chinese New Year. The lack of capacity discipline continues to pull down freight rates with the SCFI shedding 4.4% last week with carriers rolling back earlier rate increases.

The threat of further capacity surplus arising from the reopening of the Suez routes has risen following Maersk’s decision to return its ISC/Middle East-US East Coast MECL service to the Suez route from January. Further re-routings could follow the Gemini Cooperation’s IMEX/ME11 ISC/ME-Med service expected to be the next service to make the switch. The looming over-capacity crisis has not deterred carriers from adding to the already bulging orderbook with COSCO and PIL the latest to place newbulding orders while MSC is set to take a substantial number of Sinokor’s current 78 units containership fleet.

Johnson Leung

Johnson Leung

Transatlantic carriers at risk after Trump imposes 10% import tariffs

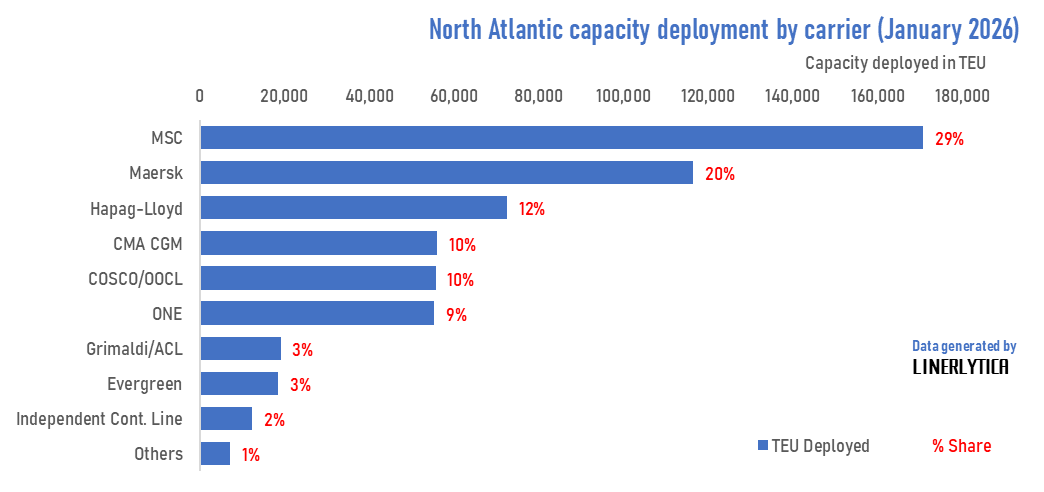

Trump announced on 17 January that eight European countries would face increasing tariffs starting at 10% on 1 February and rising to 25% on 1 June. The tariffs target Denmark, Norway, Sweden, France, Germany, United Kingdom, Netherlands and Finland if a deal is not reached on Greenland. Transatlantic container imports from North Europe to the US grew by 5.9% in 2025, but growth was already slowing in December and could be further hit by the new tariffs. The 4 main European carriers control 71% of the total capacity deployed on the North Atlantic route and would be the most badly affected by the potential fallout.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per yea