Container freight rates enjoyed a mini year end rally with the SCFI rising by 6.7% in the last reading of 2025 while the CCFI increased by a more modest 2.0%. Despite the recent rate strength, average 4th quarter CCFI rates remain 10.7% lower than the 3rd quarter and the current quarter’s rates is at the lowest level in 2 years with carriers’ earnings already under pressure.

CMA CGM has started to send their ships back o the Suez route as scheduled from last week on their eastbound voyages from Europe on the FAL 1, FAL 3 and MEX, as well as transits on both directions on the India-US East Coast Indamex service.

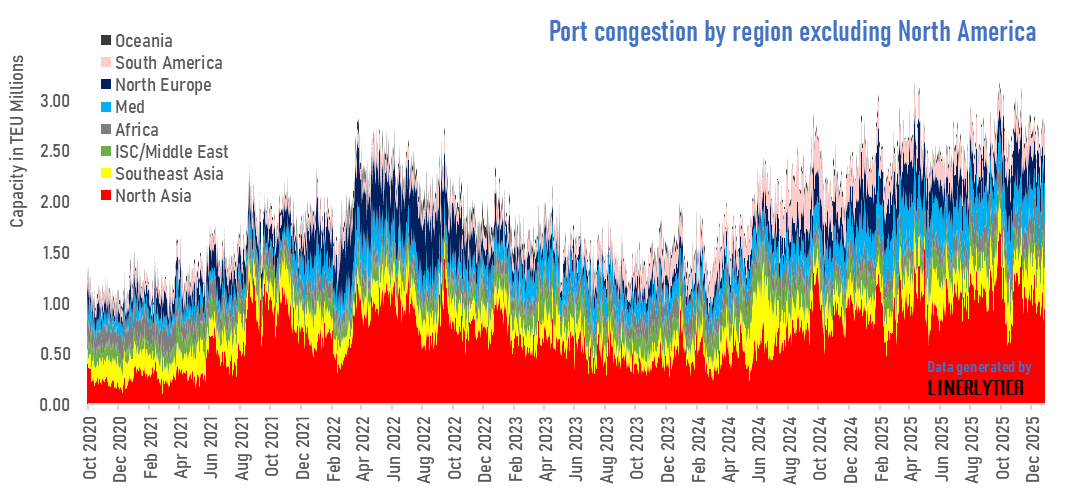

Although a full return to the Suez is still several months away, ports in Asia and Europe are already bracing for increased congestion. Outside of North America, port congestion in 2025 have already exceeded their previous peaks in 2022 and appear set to remain elevated in 2026.

Johnson Leung

Johnson Leung

Port congestion outside of North America worse now than in 2022

Congestion at container ports outside of North America reached a record high in 2025, surpassing the COVID era peaks in 2022. Ports in Europe, China and Southeast Asia all recorded heightened congestion over the past year and the number of ships waiting at anchorages at these regions remain elevated as the year end approaches. High container throughput volumes this year, coupled with unstable vessel schedules that often results in bunching of vessel arrivals as well as labour strife especially at European ports have all contributed to the increased congestion this year. Ports are bracing for worsening congestion when ships return to the Suez route in 2026.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year