Improved 3rd quarter liner earnings will reverse in the 4th quarter with average CCFI rates currently down 14% QoQ. Transpacific rates are slipping badly with capacity utilization continuing to fall on weakening demand. Although Asia-Europe rates have remained resilient, spot rates also remain under pressure with European port congestion the main factor keeping supply growth in check.

Intra-Asia rates have outperformed the long haul routes, with average shorthaul CCFI rates only down by 1% QoQ while maintaining higher volume growth. Asian carriers have performed better than their European counterparts and have retained their superior EBIT margin gap over the past year.

The recent series of new ship orders have lifted the orderbook to a new post-GFC high of 34%, further raising the forward over-supply risk with 2028 deliveries at a record 4.4m TEU with additional orders still to come.

Johnson Leung

Johnson Leung

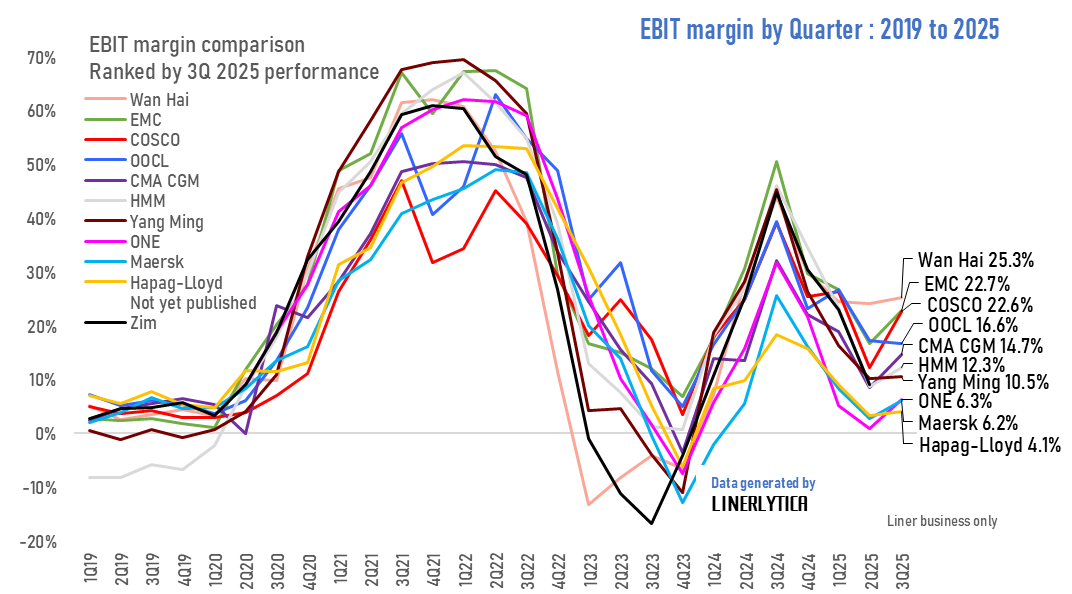

Hapag-Lloyd and Maersk earnings continue to lag behind rivals

The Gemini Cooperation partners Hapag-Lloyd and Maersk remain at the bottom of the EBIT margin ranking amongst the main publicly listed carriers, lagging behind their industry peers by as much as 20%. The high cost of maintaining the superior schedule reliability of the Gemini network and their inability to secure any freight rate premium have continued to drag down the 2 carriers’ operating performance.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year