Freight rates are softening again, reversing part of their mid-October gains after the 1 November GRI flopped as weakening slack season cargo volumes provided little rate support in the absence of capacity cuts by the carriers. Transpacific rates are coming under the most pressure due to rampant rate cutting by carriers unable to fill their ships but still reluctant to pull out capacity. Latest import data shows transpacific cargo volumes falling by 8.6% in the last 2 months. European rates are holding out better with persistent port congestion capping trade capacity and keeping utilization rates at healthier levels compared to the Pacific trades.

CMA CGM continues to test a return to the Suez route with a westbound voyage on the MEX service this week after 2 eastbound voyages on the FAL1, which could erode the fragile consensus amongst the main carriers to avoid the Red Sea.

Johnson Leung

Johnson Leung

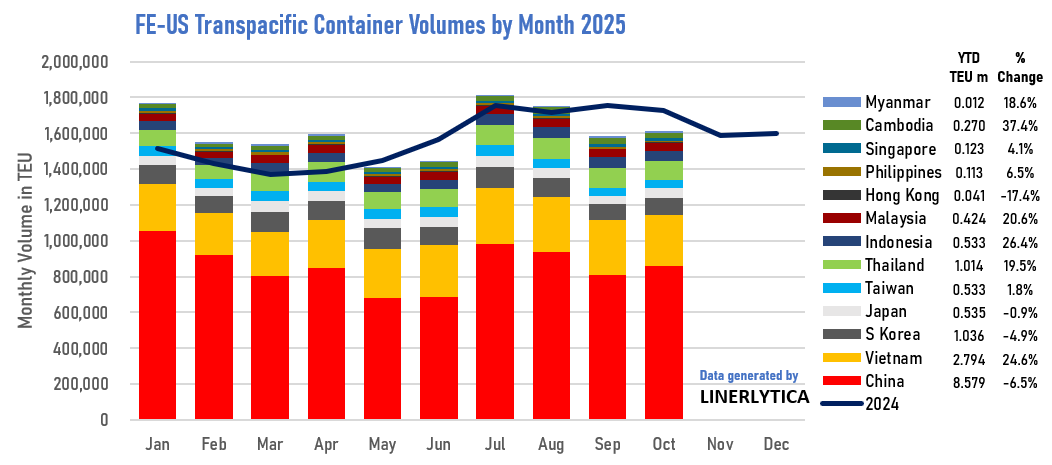

Transpacific volumes slip

Container traffic from the Far East to the US Transpacific volumes fell by 7.2% YoY in October following a 10.0% YoY drop in September. Volumes are starting to stabilize after the initial turbulence since import tariffs into the US were first announced in April this year, with the softening trend expected to continue into November and December. Although YTD volumes through October remains positive at 2.1% due to front loading during the first 4 months of this year and a strong rebound in July and August, full year volumes are expected to grow by just 0.4% and will remain largely flat for most of 2026. China’s share of Transpacific volumes has dropped with total volumes dropping 6.5% YTD while Southeast Asian origins have gained by 23.0% with Vietnam the main beneficiary.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year