US-China trade tensions eased following the broad agreement reached last week between the 2 countries including a 1 year pause on their respective port fees and a reduction in tariff and other strategic trade barriers. The ramifications on the container markets will be mixed, as the port fees were mainly targeted at COSCO and Matson and had only a limited impact on other carriers and overall global fleet deployment.

More stable trading conditions over the coming weeks could derail carriers’ rate restoration efforts which has benefitted from the recent turmoil with the SCFI rebounding by 40% over the past month. Freight rates are already retreating after their recent gains, with North Europe and US East Coast rates coming under pressure although rates to the US West Coast are still holding up despite the absence of capacity discipline.

Johnson Leung

Johnson Leung

No early return to Suez route despite CMA CGM’s FAL1 redeployment

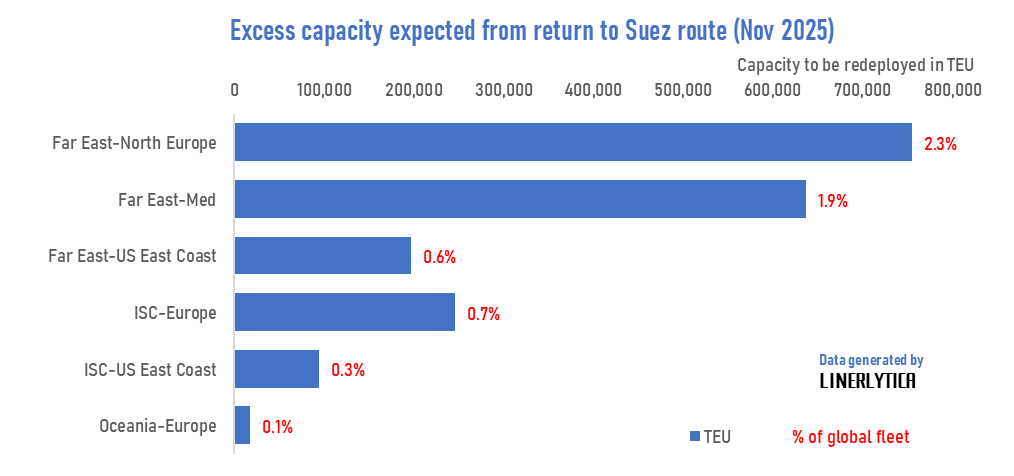

CMA CGM’s decision to send 2 of its FAL1 ships on eastbound passages on the Suez marks the first tentative steps by main line carriers to return to the Red Sea after 2 years of diversions to the Cape route. However, this move is not expected to trigger a wholesale return to the Suez in the near term as risks to vessel and cargo safety remains high. Notably CMA CGM has not diverted any North Europe headhaul ships westbound on the Suez and is only redeploying ships on selective eastbound backhaul voyages in order to bring the ships and empty containers back to Asia following severe delays at European ports recently.

If all the containerships currently on the Cape route are redirected to the Suez, it could release over 130 ships with a total capacity of 1.95m TEU or 5.9% of the global fleet which would trigger severe disruptions to the freight and charter markets.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year