The special port fees applied by the US and China on each country’s ships took effect on 14 October but the impact has been less severe than initially expected. Chinese authorities have not applied the 25% US ownership rule strictly and only Matson is affected by the fees so far although Maersk and Hapag-Lloyd diverted 2 of their US-flagged ships on the Transpacific TP7/WC5 service to avoid the port fees. At least one US-flagged operator has received waivers due to their newbuilding orders in China even though the waiver provision in the initial draft rules were omitted in the final Chinese version. The situation remains fluid with the final determination of the ownership threshold still to be announced.

These disruptions were enough to drive SCFI freight rates up by 13% last week but there is insufficient cargo volumes to support a sustained rate push.

Johnson Leung

Johnson Leung

Winners and losers from last week’s IMO vote to delay carbon pricing

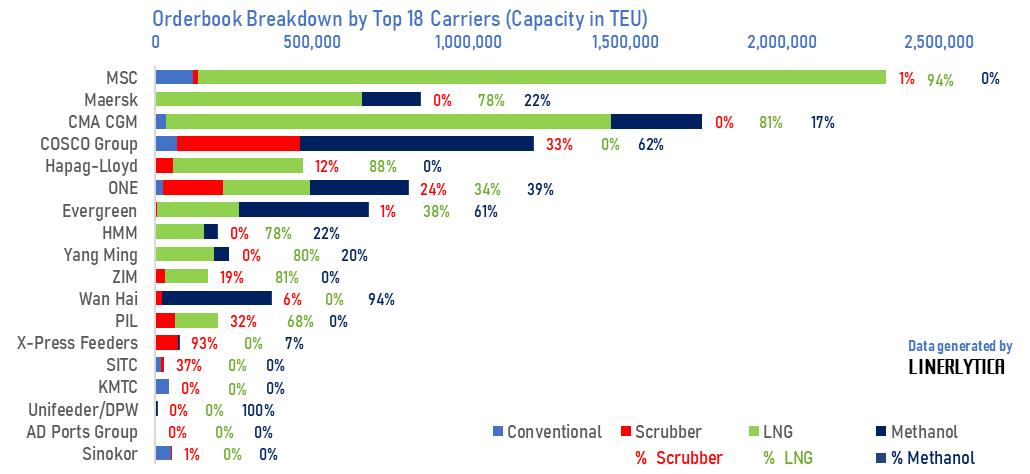

IMO member states voted 57-49 to adjourn the MEPC meeting for one year on 17 October 2025, delaying the adoption of the Net-Zero Framework (NZF) which raises investment uncertainty for new containerships although it will not stop the ongoing wave of new ship orders. Owners have added a further 240,000 teu to the orderbook in the last 2 weeks, bringing total new containership orders in 2025 past the 4m teu mark. Containership owners and operators are already ahead of other shipping segments in the adoption of green fuels, with 78% of the current orderbook capacity of 10.8m teu able to run on LNG or Methanol.

However, the NZF postponement will favour transitional fuels like LNG over methanol with carriers such as MSC set to benefit as 94% of its current orderbook are LNG powered. The NZF delay will also favour carriers with older fleets which would also benefit MSC as its average fleet age at 17 years is higher than its peer average at 11 years.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year