Extreme weather conditions in South China and North Vietnam have severely disrupted vessel schedules with elevated port congestion in the Far East persisting through the week. The disruptions failed to support freight rates which remain in freefall even as attention shifts to carriers’ mid-October rate restoration efforts to stop the bleeding. However, prospects are bleak given the weak cargo volumes and lack of capacity curbs. New US tariffs targeting kitchen cabinets and furniture will further hit container volumes already reeling from earlier import tariffs.

Operating margins have already dropped below breakeven on several key routes after the recent rate slide but carriers have continued to prioritise market share over profitability as the disconnect between charter and freight rates has widened to a record high.

Johnson Leung

Johnson Leung

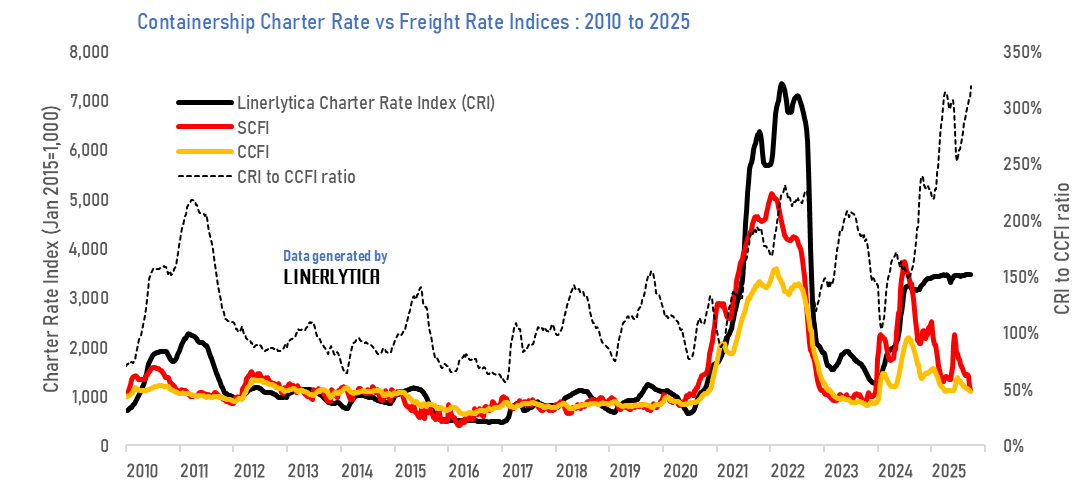

Charter rates remain elevated despite free-falling freight rates

The SCFI and CCFI have slipped by 70% and 50% respectively since their 2024 peaks, but Linerlytica’s Charter Rate Index (CRI) has continued to rise throughout this period. The CRI to CCFI ratio has reached a record high of 318%, but charter rates and second hand prices show no signs of weakening as carriers continue to chase after tonnage in an early warning that capacity management remains elusive.

The mid-October rate hikes are unlikely to succeed given the lack of capacity cuts even as the market enters the slack season. Service withdrawals for the winter season announced so far have been negligible, which could portend further freight rate weakness in the 4th quarter.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year