Although global container volumes have remained resilient so far this year, freight rates continue to be beaten down. The SCFI rally was short-lived as the composite index slumped by 14.3% last week in its 3rd worst weekly drop since 2009 as carriers gave up all their Transpacific rate gains in early September and resumed their price war ahead of the Golden Week holidays in China. Rates from China to the emerging markets were not spared, as carriers slashed rates across the board in the absence of capacity discipline.

With no substantive announcements following the discussions between the leaders of China and US last week, COSCO has already signalled their intention to match their US rivals’ rates and committed to retain their transpacific network despite the looming USTR service fee that will be implemented on 14 October, setting the stage for a protracted price war.

Johnson Leung

Johnson Leung

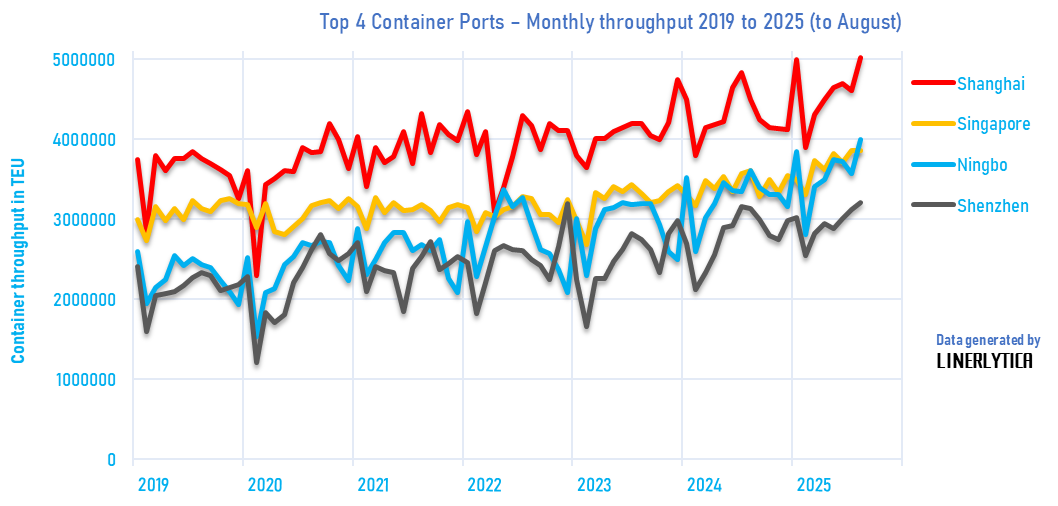

Chinese container volumes at record high despite US tariffs

Shanghai and Ningbo recorded their highest ever monthly container throughput in August, as global container volumes have remained resilient despite the gloomy trade and economic outlook. Total volumes at the 2 largest Chinese ports exceeded 5m teu and 4m teu respectively in the past month and continue to defy the impact of the US tariffs, with significant growth recorded on the Intra-Asia, Indian subcontinent, Latin America and Africa routes.

In the first 7 months of 2025, container volumes handled at Chinese ports (including Hong Kong) grew by 5.9% and the relative strength is expected to be maintained through the end of this year. Global container throughput is expected to grow by a better than expected 3.2% for the full year as the US tariffs have failed to dampen global volume growth.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year