Container freight rates resumed its decline with the SCFI slipping by 3.2% last week, with sharp drops in rates from China to Europe, Mexico, Middle East and India. Even the SCFI rate gains on the Transpacific is masking the weakness in the US trades, with market rates already falling rapidly. The suspension of 2 services to the US West Coast in September is insufficient to stop the rate rot as only 1.5% of the total capacity on the route is removed.

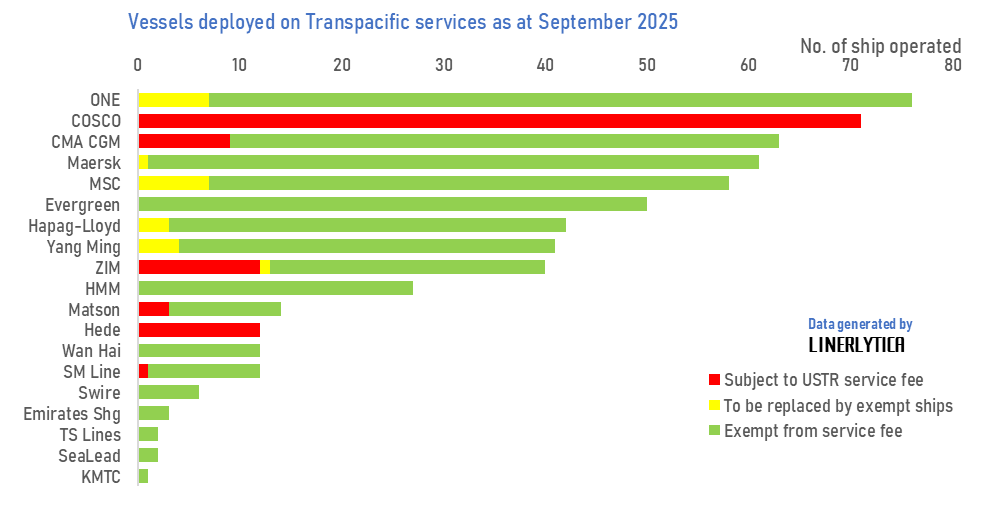

The USTR 301 service fees will not hit the Transpacific carriers equally when it comes into effect in mid-October, with COSCO set to bear the brunt of the port charge. Amongst the non-Chinese carriers, most of them will be fully exempt from the fee, with CMA CGM and Zim being the only main exceptions although their exposure to the USTR fee is only a fraction of what COSCO will incur.

Johnson Leung

Johnson Leung

Chinese carriers set to incur hefty fees on Transpacific services

With just 1 month to go before the USTR 301 service fees for ships operated by Chinese carriers take effect from 14 October 2025, COSCO and Hede have retained all of their ships on the transpacific services despite the hefty charges that they will incur. Based on Linerlytica’s analysis, COSCO would incur total fees of up to $1.02 Bn in the first 6 months of the US port charge, compared to $40m for Hede, with the fees to be progressively increased from April 2026.

Of the other transpacific carriers that operate China built ships on the transpacific, MSC, Maersk, Hapag-Lloyd, ONE and Yang Ming will shift all of their affected ships out of the transpacific trade before the mid-October deadline, based on these carriers’ forward deployment plans. However, CMA CGM and Zim have still not made moves to shift their non-exempt ships, with potential bills of up to $37m and $35m respectively in the first 6 months.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year