\Although the composite SCFI index was unchanged last week, it masked conflicting performances across various key tradelanes with the Asia-Europe route slumping to its sharpest weekly decline since February while the Transpacific route showed surprising resilience and managed to hold on to most of its 1 September rate hikes. The resilience is not expected to last, with freight rates remaining under pressure due to the lack of capacity discipline. Golden Week blank sailing programs that have been announced so far for October have been unconvincing with Gemini carriers unwilling to withdraw surplus capacity and are prepared to slash rates to maintain schedules.

New containership orders continue to ratchet upwards, with the orderbook reaching 32.2%, and planned deliveries will hit 2.9m teu in 2027 and 3.8m teu in 2028. The new deliveries will far exceed the projected scrapping of older vessels in the coming 3 years.

Johnson Leung

Johnson Leung

Surge in new containership orders continues

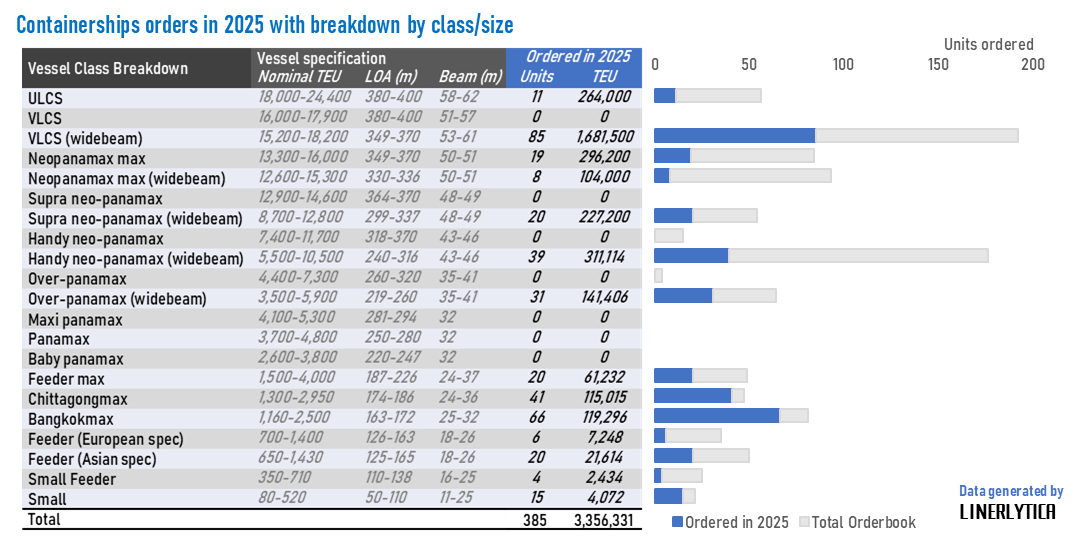

The number of new containerships ordered in the first 9 months of 2025 has reached 385 units for 3.36m teu. Full year numbers could match the record of 4.67m teu ordered in 2024 and 4.74m teu ordered in 2021 if the current pace of new ship contracting continues. The widebeam VLCS segment of 15,000-18,000 teu (LOA of less than 370m) has become the most popular vessel size with 85 units added this year to the orderbook that now stands at 192 units. Feeder ships of below 4,000 teu are also in favour with 172 units added this year, of which 66 are Bangkok-max units.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year