The SCFI staged its first rebound after 11 consecutive weekly declines but the rebound will be short lived as freight rates will resume their downswing in the absence of capacity cuts by carriers. The market continues to be in a stand-off with the planned September rate hikes not expected to hold as carriers shift their focus to filing their excess vessel capacity and building up cargo roll pools ahead of the Golden Week holidays in China in October.

While the freight rate outlook remains negative, charter rates continue to hold firm with vessel availability still very tight despite the recent rise in the idle fleet that was driven solely by the addition of OFAC sanctioned ships over the past month. Declining freight rates and rising operating costs have pushed average carrier earnings to 8.4% in the 2nd quarter, with further margin erosion expected in the next 2 quarters that will push carriers earnings into negative territory once again.

Johnson Leung

Johnson Leung

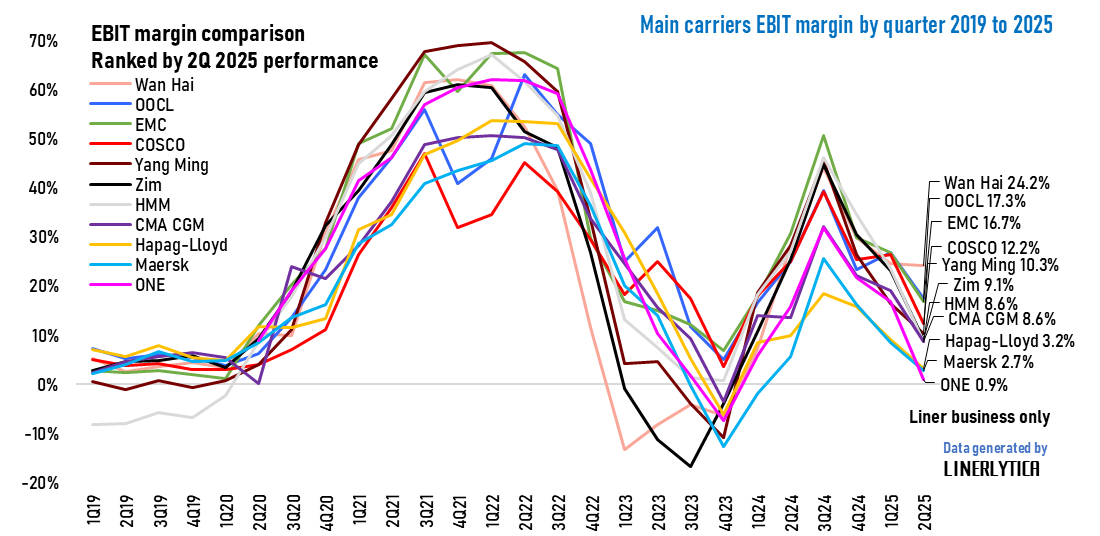

ONE and Gemini partners remain stuck at bottom of carrier earnings ranking

Carriers’ average EBIT margins dropped to 8.4% in the 2nd quarter of 2025, but the gap between the top and bottom performers remain very large with Asian carriers continuing to outperform their European peers. ONE was the key exception amongst the Asian carriers, with the lowest EBIT margin at 0.9% due to accelerating operating costs. Maersk and Hapag-Lloyd remain at the bottom quartile with the launch of the Gemini Cooperation network in February doing little to lift the 2 partners’ competitiveness vis-à-vis their main rivals.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year