Revised US tariffs that will take effect on 7 August will have a negative impact on overall global demand even though the average tariff rates were lower than initially announced on 2 April. Although global container growth projections have been revised upwards, over-supply pressure persists with freight rates remaining under pressure after the SCFI extended its losing streak to its 8th consecutive week. Further rate declines are expected throughl October, with prospects for a seasonal year-end rebound still uncertain despite EC freight futures pricing in a minor recovery at the year end.

The US crackdown on containerships owned by Iranian interests will have a limited impact on the East Med and Red Sea routes that are temporarily disrupted due to the withdrawal of 16 ships operated by Sealead that were added to the sanctions list last week. An additional 6 ships operated by Vuxx on Russian routes have retained their deployment for now. The charter market remains extremely tight with the idle fleet hitting a 2 year low.

Johnson Leung

Johnson Leung

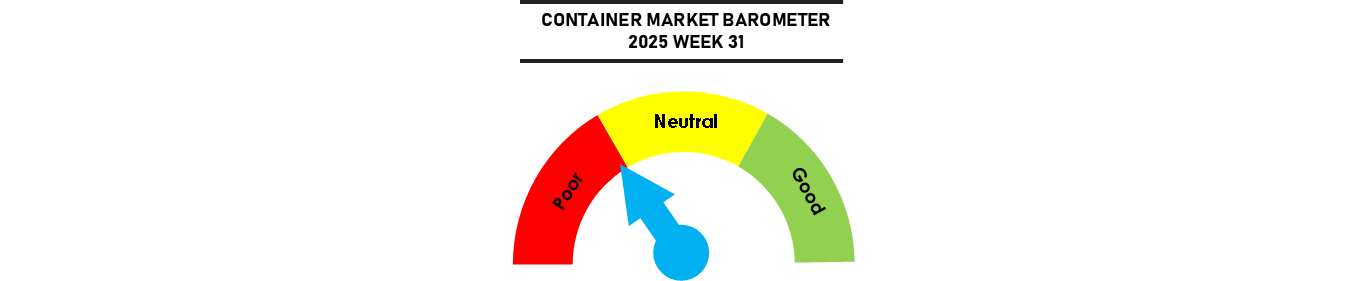

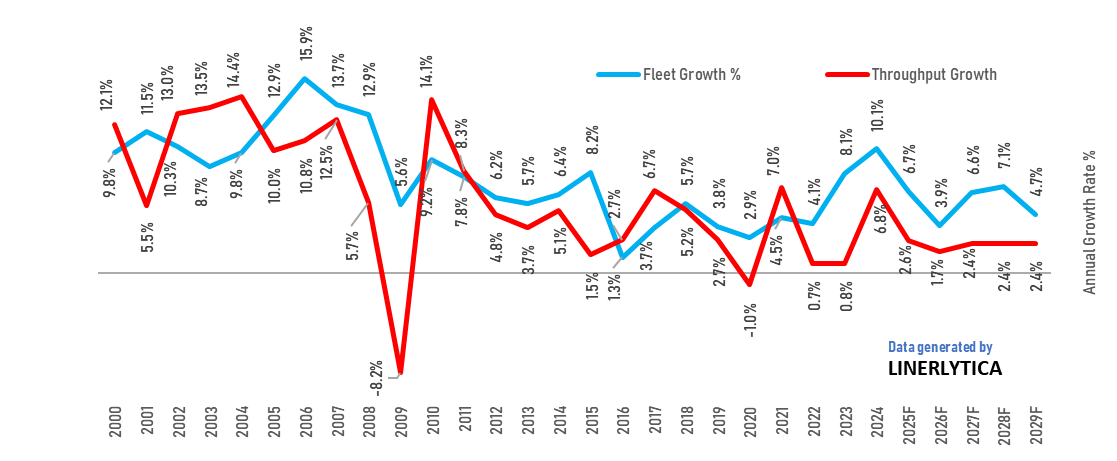

Excess capacity persists despite upward revision in global container demand

Global container throughput growth have been revised upwards and is expected to grow by 2.6% in 2025, in line with the IMF’s revised global GDP growth outlook released last week due to cargo front loading during the first half of this year, lower effective US tariff rates, improved financial market and government fiscal stimulus by several key countries.

Despite the revision, the US tariffs have already spurred higher inflation and slower job growth which will lead to slower growth in the 2nd half of 2025, with the lower growth rate expected to carry over into 2026 with global volume growth expected to slow to 1.7%. The bigger challenge will come from the supply imbalance as the containership fleet growth will continue to outpace demand growth, with excess supply projected to persist through 2029.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year