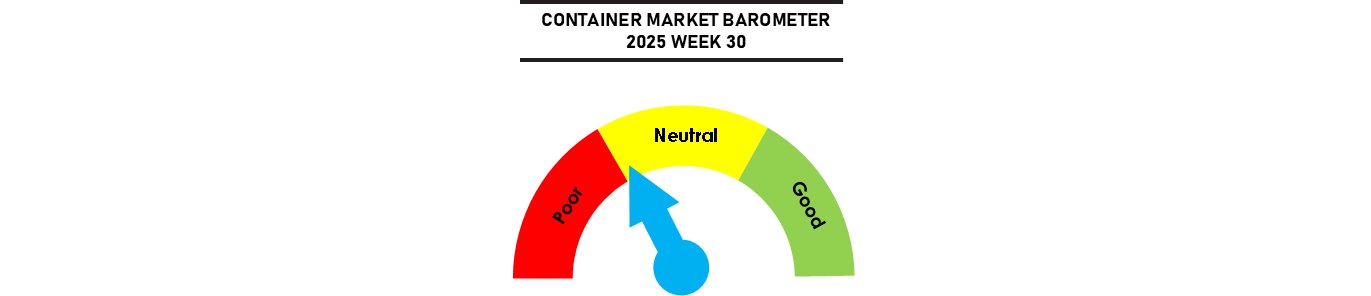

Global container throughput growth has remained resilient in the first half of this year, with total volumes growing by 5.3% with all regions apart from Oceania recording positive growth in the first 6 months of the year. However the outlook for the second half is more gloomy, as cascading impact of US tariffs start to affect container volumes negatively. The US-EU trade deal is expected to hit Transatlantic westbound freight rates, with US imports expected to drop by more than 10% even though the 15% tariff on EU goods is not as steep as Trump had initially threatened. Container imports from Europe to the US increased by 8% in the first 6 months of the year, but the growth is projected to reverse in the second half. Total capacity deployed on the Transatlantic route is up 16% YoY and this too could reverse over the coming year.

Overall freight markets remain weak, with the SCFI dropping for its 7th consecutive week, with planned August rate hikes failing to stick as capacity continues to trend above demand.

Johnson Leung

Johnson Leung

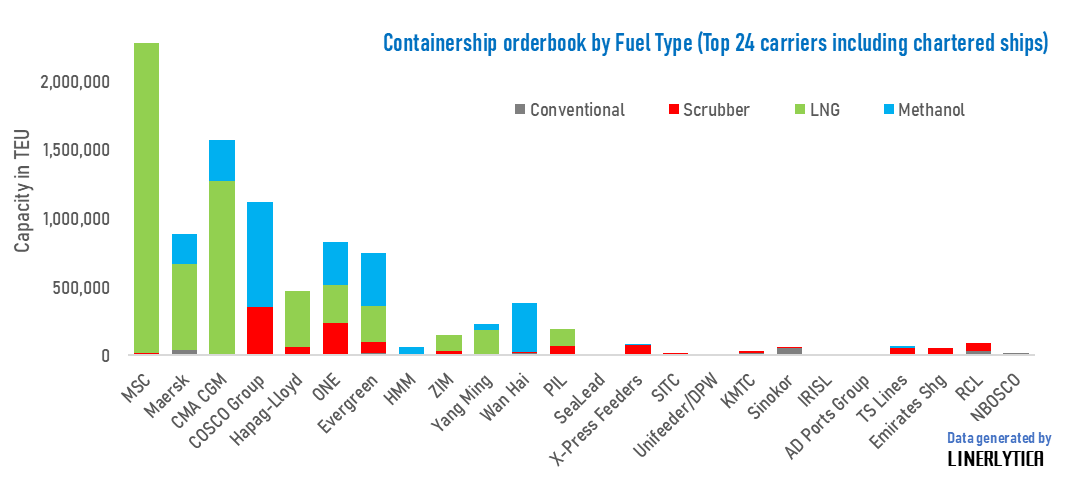

Carriers’ appetite for new ships remain unabated

271 new containerships for 2.6m TEU were ordered in the first 7 months of this year, not including undeclared options that would raise the final tally to over 300 ships as carriers’ appetite for new tonnage remains unabated. The wave of new orders is not about to end soon, with attention shifting to feeder sizes. The orderbook for ships of below 4,000 teu currently stands at just 6.8% of the current fleet, compared to 16.2% for ships of 4,000 to 10,000 teu, and 51.7% for ships of over 10,000 teu.

MSC continues to lead the race for new ships, opting for a predominantly LNG orderbook while its main rivals have mostly chosen a mixed orderbook comprising of both LNG and methanol fuel ships.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year