Container freight rates continued their precipitous fall as the SCFI shed a further 5% last week with weaker rates across all main trades led once again by the Transpacific. Carriers’ reluctance to withdraw surplus transpacific capacity amidst the tariff chaos doomed their mid-July rate hike efforts. Rates to North Europe that have held up well in the last 2 months are also starting to crack with vessel utilization rates dropping noticeably last week, potentially signaling an early end to the peak season.

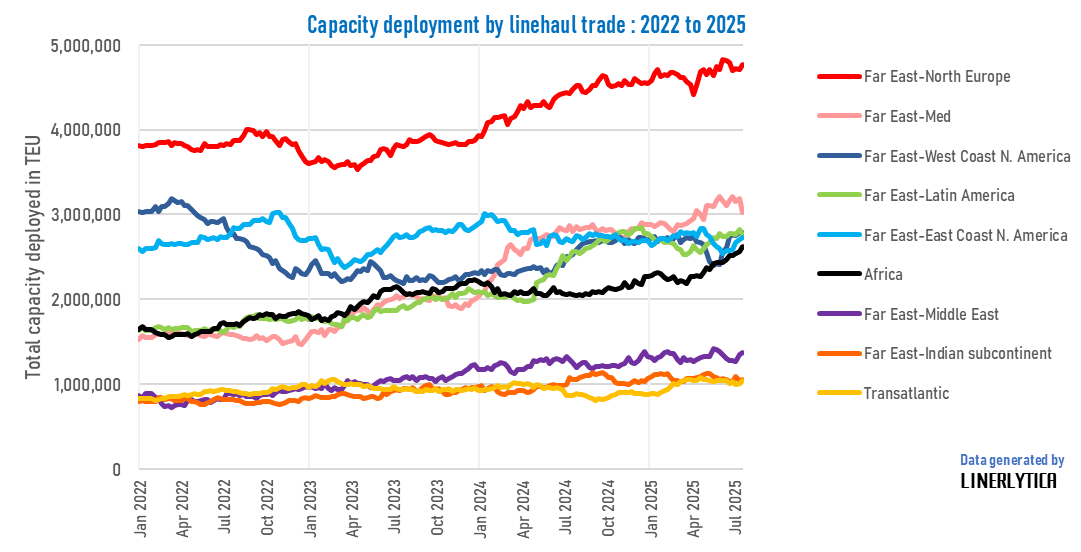

Charter rates have continued to hold firm, with carriers making no efforts to cut back on their capacity deployment despite the deteriorating freight rates. Second hand vessel transactions and new vessel orders remain very strong with MSC once again leading the charge. African trades are coming under the limelight with the largest capacity influx in the last 12 months, absorbing a quarter of the net capacity additions since July 2024.

Johnson Leung

Johnson Leung

African routes leads capacity influx in last 12 months

Global containership capacity has risen by 2.43m TEU in the last 12 months, registering a growth of 8.1% YoY with 2.48m TEU of new vessel deliveries added against just 0.05m teu that were scrapped. African routes helped to absorb 23% of the net capacity additions with 0.57m teu added on the trade since July last year. MSC’s redeployment of their 24,000 teu ships to the FE-West Africa trades since March have played a key part in the rise of African vessel capacity and relieving the capacity overhang on both the Asia-Europe and Transpacific routes.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year