The SCFI rolled back all of the gains of the past 3 weeks as Transpacific rates collapsed under the weight of excess capacity. Freight rates to the US West Coast have recorded their largest weekly losses in the last 2 weeks as their failure to retain any of their 1 June rate hikes have also put the peak season surcharge for contract customers at risk. The early end to the transpacific peak season have not yet dragged down rates on the secondary routes that remain supported by buoyant cargo volumes, while charter rates also remain firm with very limited open tonnage. However cracks are starting to appear with EC freight futures for August trading below June prices, suggesting that the market may have already reached its peak for this year.

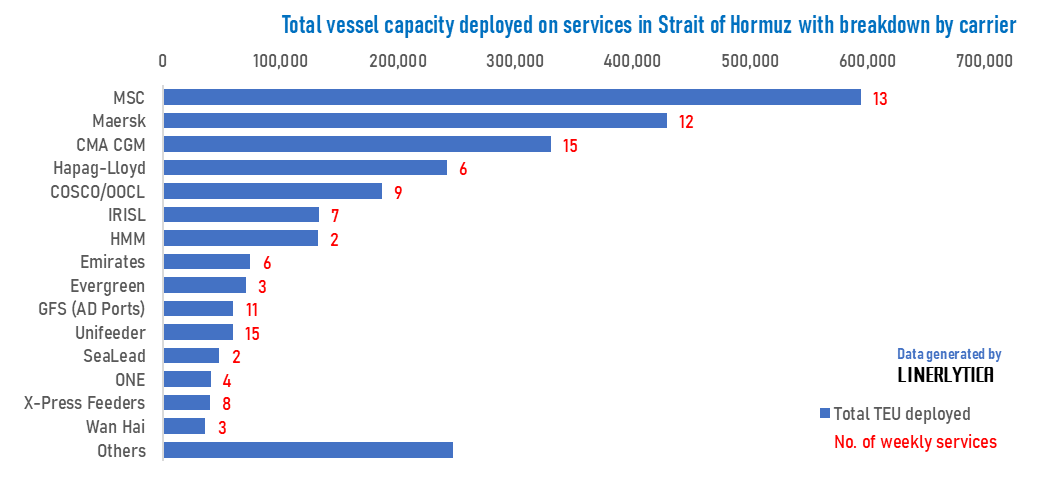

The likelihood of Iran following through on its threat to close the Strait of Hormuz is low as it would affect not just its oil exports but also its container imports with over 35% of its container cargo transhipped through other Middle East Gulf ports.

Johnson Leung

Johnson Leung

Strait of Hormuz closure will also cut off Iranian cargo supplies

Despite Iranian threats to close the Strait of Hormuz to vessel traffic, such a move would also cut off supplies to Iran. Apart from container shipping services operated by IRISL and several smaller Iranian carriers that call directly at Iranian ports, a significant part of Iranian container traffic is also transhipped through other Middle East Gulf ports, accounting for over 35% of the 2.5m TEU handled at Iranian ports in 2024.

Total container vessel capacity operated on services that passes the Strait of Hormuz currently stands at 3.2m TEU, accounting for 8.4% of the global fleet but there are no Israeli or American owned ships currently deployed on this route.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year