Fears over a container market correction sparked by the possible end to hostilities in the Middle East proved to be premature as Chinese freight futures regaining all of last Tuesday’s losses, with further gains still to come after the SCFIS recorded a 3rd straight week of double digit % gains. The introduction of 3 new Asia-North Europe strings in June and July has not dragged down freight rates with further hikes still planned in the coming weeks as blanked sailings arising from the current schedule disruptions continue to put a cap on vessel departures in the next 6 weeks. Port congestion continues to rise, with German ports set to become the next hotspot after an unannounced strike action was declared on 17 June which will further exacerbate schedule disruptions especially on the Asia-Europe route. Transpacific demand is also enjoying a similar uptrend especially to the PSW with the incremental capacity from new services launched and extra loaders fully taken up with at least 2 more rounds of rate hikes still to come.

Johnson Leung

Johnson Leung

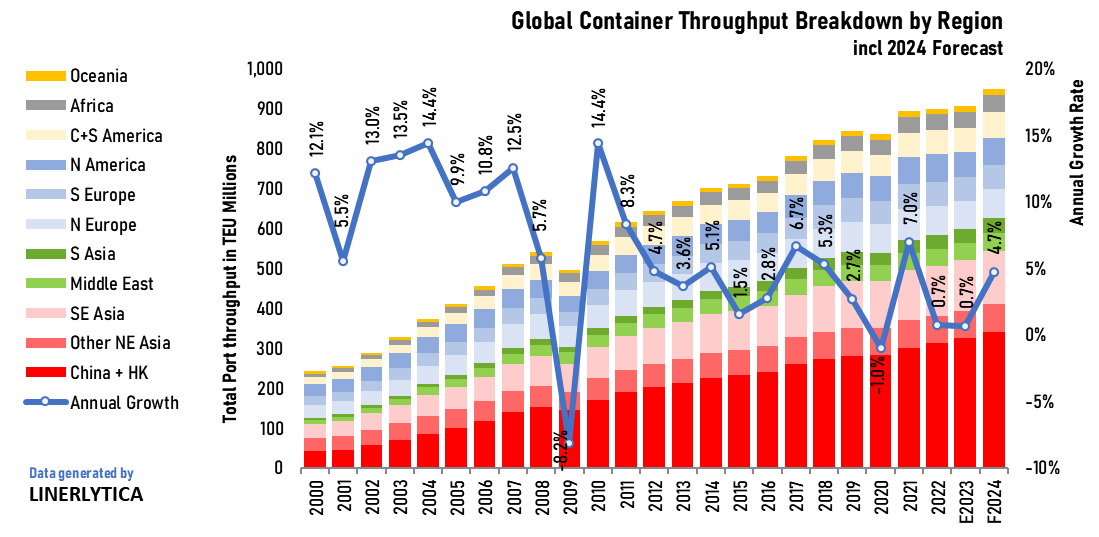

Container volume growth forecast revised upwards

Global container port throughout is expected to reach a record high of 947m teu in 2024, with full year growth forecasts revised upwards to 4.7% following 2 consecutive years of lacklustre growth of 0.7% in 2022 and 2023. The sharp rise in cargo volumes in the first half of 2024 has propelled port congestion to a new 18 month year high, with notable gains at several key Asian hubs including Singapore (up 7.7% YTD), Tanjung Pelepas (up 20.1% YTD) and Colombo (up 20.4% YTD).

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year