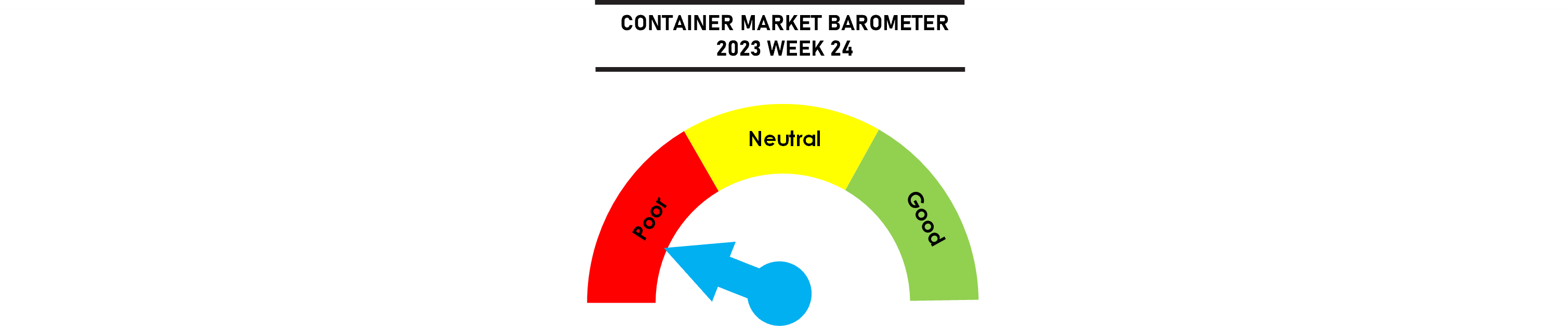

The SCFI slipped by 4.7% last week on the back of slumping transpacific rates with carriers slashing rates on both the West Coast and East Coast routes, erasing all of the recent GRI gains. The US west coast dock labour dispute remains a distraction with only a minimal impact on vessel operations and latent congestion already easing, while the Panama Canal draft restrictions failed to stop rates from falling on the east coast with sufficient vessel capacity still available. Capacity utilisation remains too low to support rate increases, with the planned 15 June rate already withdrawn by most of the transpacific carriers, with the next attempt to raise rates deferred to 1 July. However, transpacific volumes have remained persistently weak especially to the US west coast. Even the strong demand on European routes has failed to stop rates from dropping, although rates to the Med has proven to the most resilient.

Johnson Leung

Johnson Leung

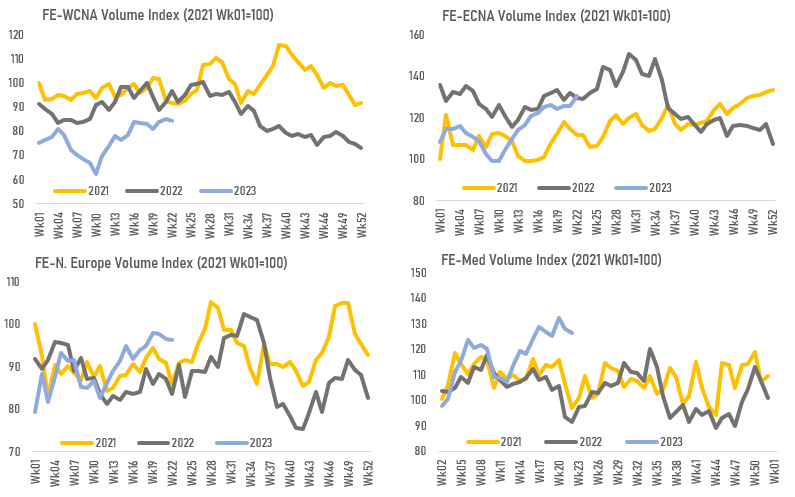

Linerlytica’s trade volume index, calculated from vessel capacity and utilization data, shows continued weakness on the transpacific routes heading into the summer peak season but European routes have enjoyed a revival with the Asia-Med trade particularly strong with the current volume index up by more than 30% compared to last year.

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year