The global containership fleet has passed 28m teu last week, with total new ship deliveries since the start of this year reaching 1.94m teu. More than 1 new ship has been delivered each day since June this year, with the same pace to continue through the next 12 months. Carriers are facing a difficult time maintaining recent freight rate gains in the face of the capacity influx, with vessel scrapping and idling remaining at very low levels. Although ships in drydock has increased with a new wave of vessel upgrades in place, this will come at price as it reduces the pool of ships to be scrapped in the near term.

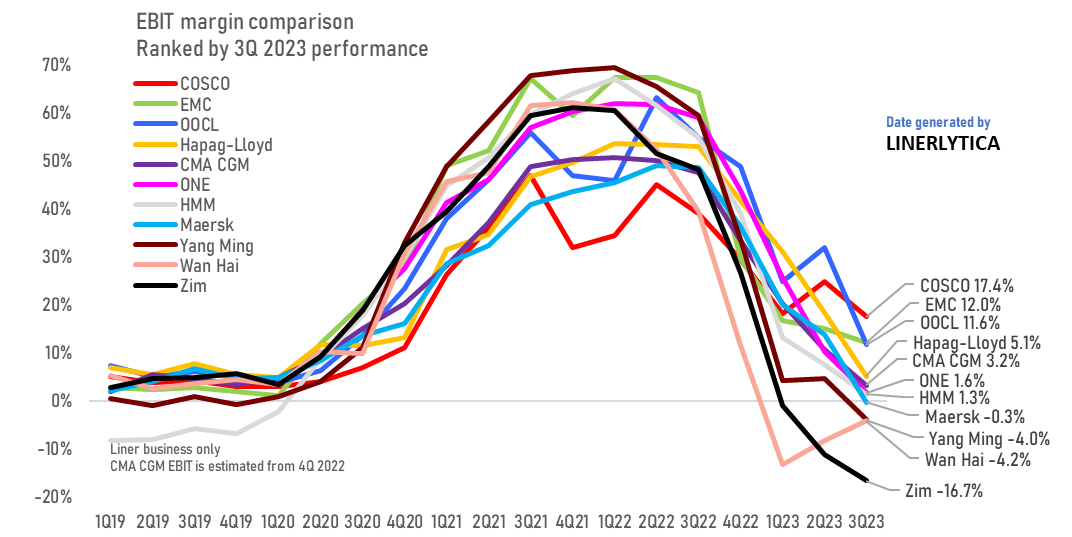

Illustrating the challenges that carriers are currently facing, Zim’s fruitless efforts to contain its operating losses continues despite taking a $2Bn impairment charge in its most recent financial quarter but it is still not enough to return the carrier to profitability in the 4th quarter.

Johnson Leung

Johnson Leung

Zim’s $2bn impairment will not be enough to lift its 4Q performance

Zim recorded a net loss of $2,270m in the 3rd quarter, due mainly to a non-cash asset impairment write down of $2,063m. Adjusted EBIT losses excluding the non-cash items stood at -$213m for an EBIT margin of -16.7% which places Zim at the bottom of the carrier EBIT margin rankings for the 2nd consecutive quarter. Zim will receive a boost to its earnings of over $150m per quarter as a result of the impairment charge due to lower depreciation expenses going forward but it will not be enough to lift its 4Q performance to positive territory with the company expecting full year EBIT losses of between -$400m to -$600m from the cumulative 9 month EBIT loss of -$373m.

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year