Container freight rates are dropping at a faster rate than expected with the SCFI slipping below 1,000 again, giving up all of the gains made in the last 7 weeks. Weak peak season volumes coupled with oversupply across the main markets have weighed down heavily on rates with little chance of a reversal until November at the earliest. Carriers inability to curtail supply remains the biggest challenge, as capacity utilisation have weakened particularly on the US East Coast and the Med with rates on both of these routes falling sharply over the past week.

Despite an increase in the number of blanked sailings out of China scheduled for October, there are no permanent service withdrawals announced so far and the idled tonnage remains stubbornly low at just 0.4% of the current fleet. The delayed entry of several new ships of 15,000-24,000 teu has not slowed the pace of supply growth with net deliveries still running at over 180,000 teu a month.

Johnson Leung

Johnson Leung

Maersk isolation intensifies as MSC and Zim deepens cooperation

MSC and Zim have announced on 6 September 2023 a new operational cooperation agreement covering the trades between the Indian subcontinent with the East Mediterranean, the East Mediterranean with Northern Europe, and services connecting East Asia with Oceania. The cooperation is expected to be expanded when the current 2M-Zim collaboration is dissolved from January 2025, with MSC poised to further extend its current slot sale agreement with Zim on the Asia-PNW route to cover the Asia-US East Coast and Asia-Med trades.

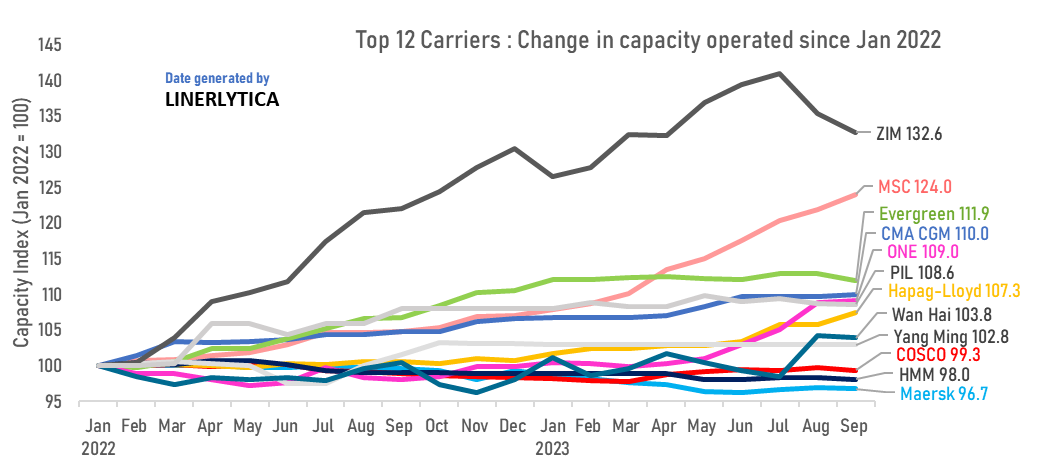

These moves will further isolate Maersk who will be left without any alliance partners on the Transpacific and Asia-Europe routes that could curtail its network coverage and access to incremental vessel tonnage. Overall Maersk capacity operated has shrunk by 3% since 2022 compared to Zim and MSC that have grown by 33% and 24% respectively.

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year