The extension of the US import tariff pause to 1 August has not helped transpacific freight rates that retained their downward trajectorory with cargo demand still slipping from the June peak. Carriers are retaining most of their transpacific capacity through the end of August despite the collapse in freight rates. The rate weakness is spreading to the East Coast with the widening gap to the West Coast rapidly eroding.

In contrast, European routes have been surprisingly resilient, with EC futures trading up on the back of spot rate hikes with capacity remaining tight following the recent bout of severe congestion at North European main ports. The US threat of secondary tariffs on countries doing business with Russia is unlikely to alter container trade flows, with the Russian market already weakening since the first quarter of this year that have resulted in the withdrawal of several Russian operators.

Johnson Leung

Johnson Leung

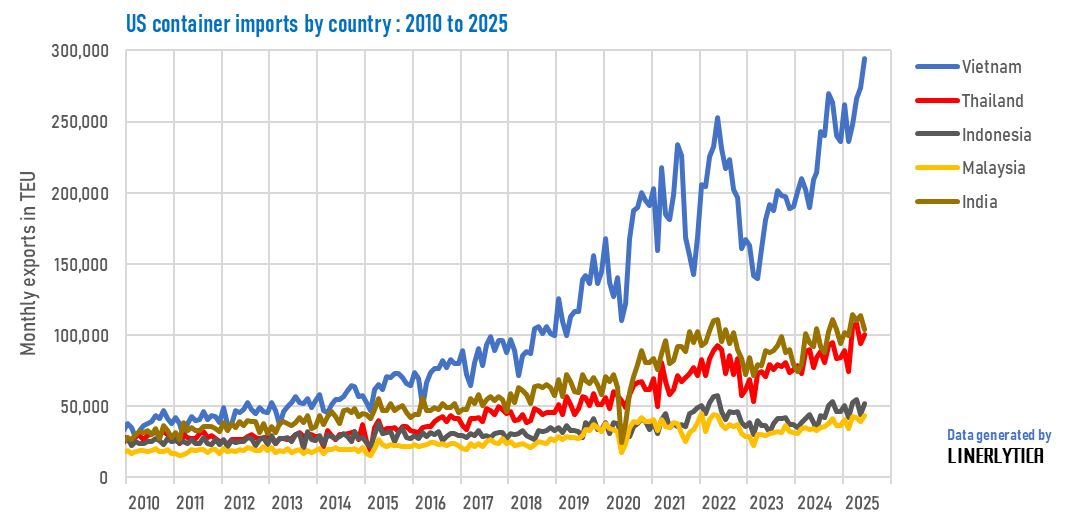

Vietnam and India set to be key beneficiaries of Trump tariffs

The new US import tariffs that are set to imposed from 1 August will not have any detrimental impact on volumes from Vietnam and India who are both set to be the main beneficiaries of the Trump tariffs as Transpacific container cargo volumes continues to switch away from China to alternative origins. Containerised exports from Vietnam to the US have risen by 29% in the first 6 months of 2025, with volumes reaching a record high in the last 2 months. Chinese exports to the US dropped by 0.8% during the same period. The 20% tariff on Vietnamese exports that will be applied from August will not materially dampen demand as the tariff remains the lowest amongst its main rivals in the Asian region.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year