The rapid decline in Transpacific freight rates have forced some carriers to roll back their capacity plans but with tonnage already committed in some cases, carriers are still pushing ahead with new Transpacific service upgrades. Emirates is the latest newcomer to the US market, making a return to transpacific after a 17 year absence, even though another newcomer CU Lines have given up plans to revive its US service after just a single sailing. Niche carriers Hede and SeaLead are still adding new capacity to the US in July even as rates falter. Average weekly capacity to the US West Coast have risen to 345,000 teu in June from 290,000 teu in April and May, and will rise further to 380,000 teu in July which will prove too much for the market to absorb, with cargo demand to the US slowing down as the tariff pause ends on 9 July.

Tradelanes outside of the US retain some stability, with freight rates still largely holding even though EC freight futures continue to suggest the market has likely reached its peak and will begin to slide from July.

Johnson Leung

Johnson Leung

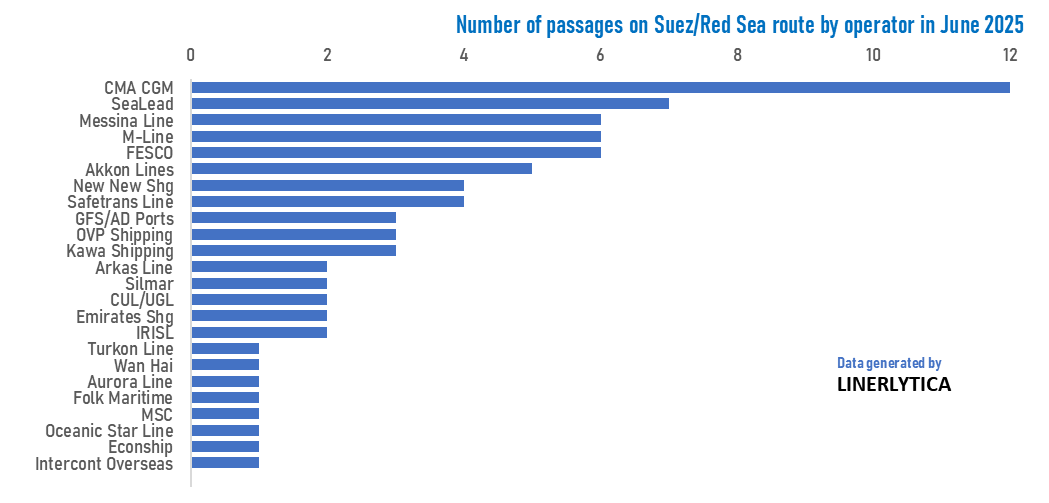

CMA CGM the only main carrier to make return to Suez/Red Sea route

CMA CGM leads the list of carriers on the Suez/Red Sea route with 12 containership passages in June. Apart from regular passages on its Asia-Med Phoenician Express and Levant-Middle East Express services that have retained their Suez routing since last year, CMA CGM added 3 ad-hoc sailings last month, including the first of the Middle East-Med Express ships that will resume full Suez passages from the end of June. CMA CGM was the only main carrier to enjoy the Suez Canal Authority’s 15% discount on transit fees for ships exceeding 130,000 in net tonnage starting from 15 May 2025 for a period of 3 months. Apart from smaller carriers on the Asia-Med and Asia-Baltic routes that have maintained their Suez transits, none of the other main carriers have added Red Sea/Suez transits since the SCA discounts were announced.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year