Several new long haul services have been launched in June, including the notable return of SeaLead to the US and BAL to Mexico that followed Ellerman’s return on the Asia-Europe route last month. COSCO and Hapag-Lloyd have also been actively adding new services on the transpacific and Asia-Europe routes. Market sentiment is clearly rising, as seen by the IPO filing by TS Lines while Maersk’s revision of its full year profit guidance only affirms what the market already knew. All these are reminiscent of the COVID bull run of 2021 but this time it’s all due to Red Sea crisis that has upended the supply-demand balance while also spurring the return of port congestion and box equipment shortages.

The SCFI gained a further 4.6% last week but spot freight rates are poised to secure several more rounds of rate hikes through August, with Asia-Europe freight futures rising to record highs last week. Charter rates also surged to fresh highs with CMA CGM reported to be paying over $100,000/day for a 3 month charter for a TS Line 7,000 teu newbuilding.

Johnson Leung

Johnson Leung

Seasonal demand pickup could last until August

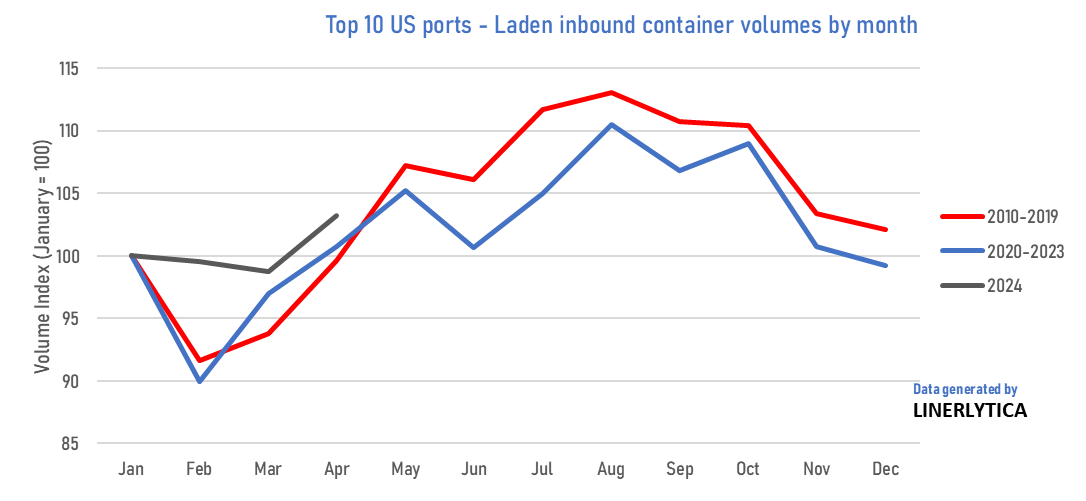

The tight container market is expected to last for at least 3 more months, as monthly container cargo volumes could rise by a further 5% to 10% due to seasonal demand which historically peaks in August based on the analysis of cargo volumes at US ports over the last 15 years. The strong cargo volumes this year has caught the market by surprise, but the peak season cargo surge could bring further pain to the market already over-stretched by a shortage of vessel capacity and box equipment.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year