Freight rates to Middle East and Latin America were the main bright spots for carriers, as SCFI recorded its first weekly increase in 2 months. However, the marginal 0.8% rise last week masked weakening market sentiment where both Asia-Europe and Transpacific rates are still under pressure, with some carriers planning another series of FAK rate hikes mid-April to stem the decline.

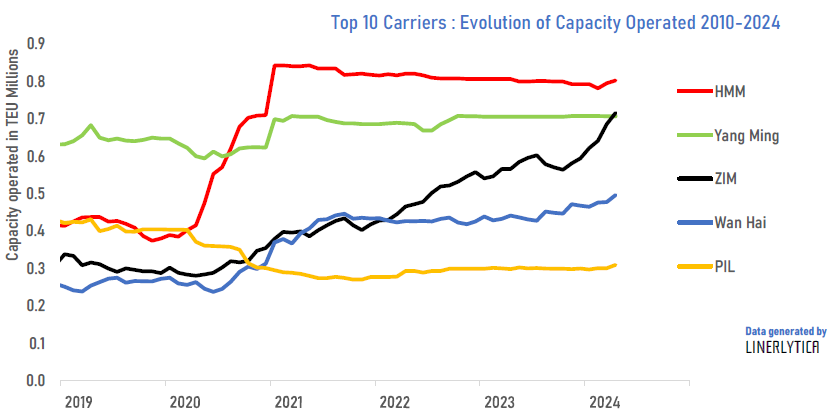

Charter rates remain buoyant with several carriers still chasing tonnage, with momentum still building after the Easter holidays. Capacity competition between carriers remain very keen, as shown by Zim’s growth since 2020. New vessel deliveries at more than 1 ship delivered daily since March will continue with over 300,000 teu scheduled to be delivered each month in April through June.

Johnson Leung

Johnson Leung

Zim moves up the ranks as it overtake Yang Ming in global capacity operated

Zim has received the ZIM MOUNT VINSON on 3 April, the last unit in the series of 10 ships of 15,248 teu built by Samsung H.I. for Seaspan. These 10 ships have been chartered by Zim for 12 years and brings its total capacity operated to 714,800 teu, lifting the Israeli carrier over Yang Ming to 9th spot in the global carrier rankings. Zim has more than doubled its size since 2020, growing by 155% over the past 4 years. Its operated fleet will be further bolstered by the delivery of 19 more new ships scheduled before the end of this year.

In contrast, Yang Ming had started as the 8th largest operator in 2020 but it has since been overtaken by both HMM and Zim with capacity stagnant and additions are due until 2026.

Register Free Trial

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year