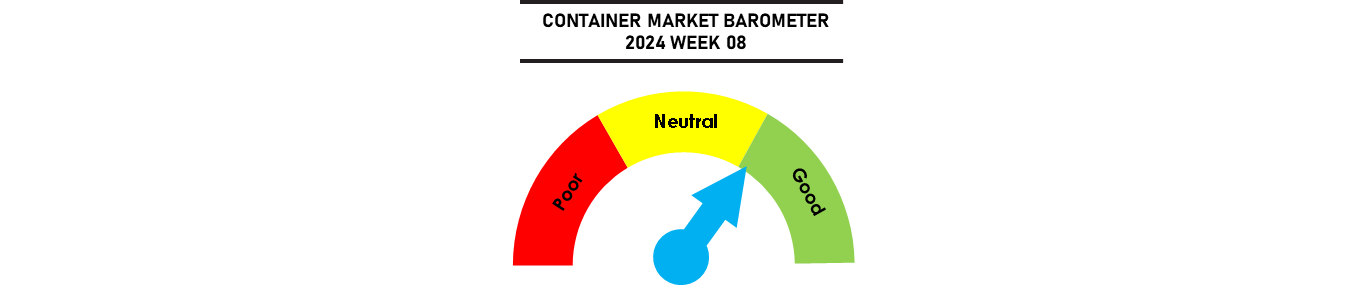

The bullish market sentiment has not been dampened by the Lunar New Year break with carriers still retaining most of their recent rates gains, defying the predictions of a post-holiday correction. Capacity is expected to remain tight in March due to the extended Red Sea diversions, with charter rates continuing to firm due to limited vessel availability. Unlike previous years when the idle fleet rises due to the post-holiday blanked sailings, carriers are able to keep their fleet fully employed with ships returning via the Cape delaying their arrivals to Asia in order to avoid the immediate post-holiday window.

The rebound in transpacific demand has also provided another reason for optimism that will keep the overall capacity tight at least for as long as the Red Sea diversions persist.

Johnson Leung

Johnson Leung

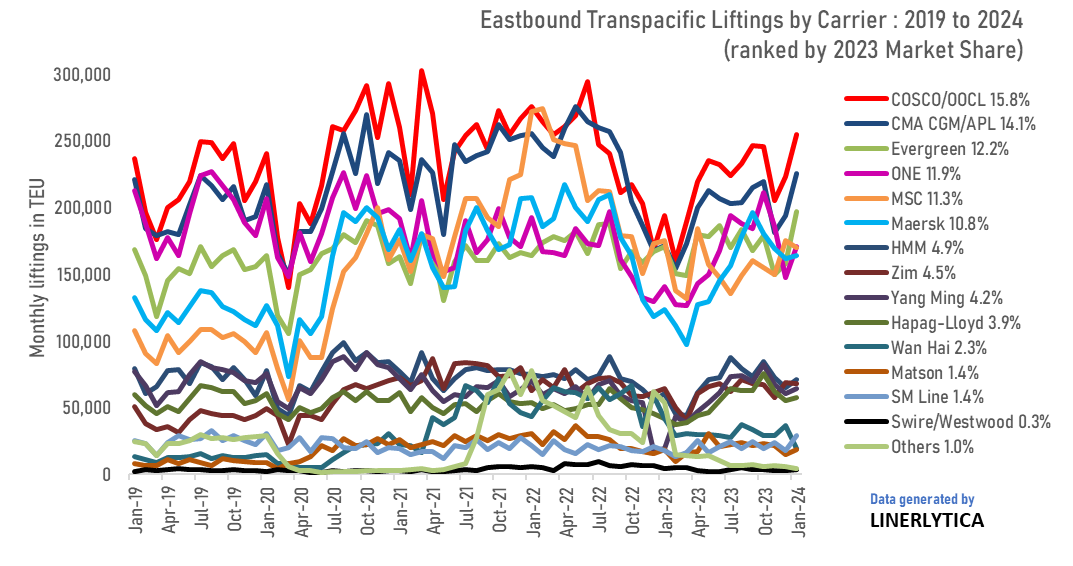

Transpacific trade growth rebound

Transpacific eastbound container volumes have rebounded by 16.9% in January 2024 and full year volumes are expected to record positive growth again after falling by 15.1% last year. Transpacific carriers have been able to take advantage of the strong cargo rebound with freight rates more than 200% higher compared to last year. The Top 3 carriers (COSCO, CMA CGM and Evergreen) have managed to retain their positions in January, and all 3 are members of the OCEAN Alliance who are poised to strengthen their dominance on the Transpacific trade with the imminent split of the 2M and departure of Hapag-Lloyd from THE Alliance in 2025.

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year