Freight rates slumped for the 2nd successive week, with the SCFI losing over 9% in the last 2 weeks as carriers continued to slash rates on the transpacific routes. The resolution of the ILWU contract negotiations will further weaken the transpacific rate outlook as the risk of any peak season disruption to cargo flows to the US is materially reduced.

Carriers need to reduce their capacity deployed to stop the rate collapse but their options are severely limited with the influx of new tonnage gathering pace as new containership capacity delivered has reached a new record high of 256,000 teu over the last 4 weeks compared to deletions of just 15,680 teu,. Meanwhile, the idle fleet continues to shrink to just 100,000 teu compared to over 1 million teu that was inactive in February.

Johnson Leung

Johnson Leung

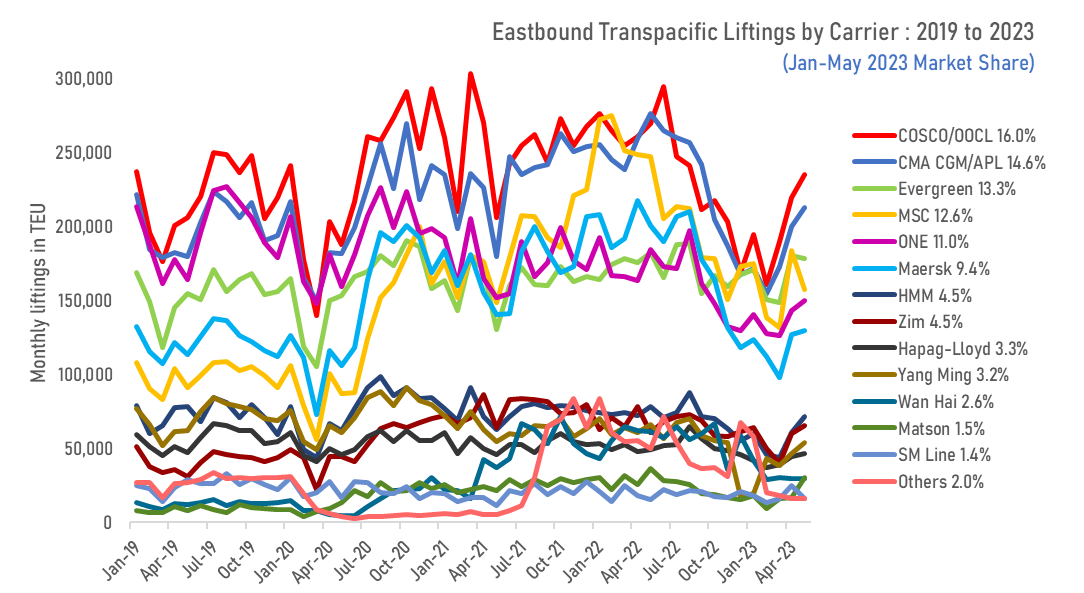

Transpacific freight rates are expected to drop further as the Asia-US trade has become the new battleground for carriers as the rate war intensifies while casualties have already started to pile up. CU Lines and Pasha are the latest carriers to exit from the trade, following the earlier departure of niche carriers such as Transfar, TS Lines, SeaLead, BAL, CIMC and Jinjiang Shipping. The micro-carriers’ share of the transpacific trade will soon drop below 1%, from a peak of 5% in December 2022. Amongst the incumbent carriers, COSCO, CMA CGM and Evergreen continue to battle for the top spot after MSC, ONE and Maersk slipped down the rankings.

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year