Market sentiment turned negative ahead of the Labour Day holidays, with the SCFI dropping by 3.6% in the last week of April, reversing part of its mid-April gains. Charter rates and second hand containership prices continued to strengthen despite the softening freight rates heading into the summer season with significant uancertainty over the direction that the market will take in the next 3 months amidst growing indications that this year’s peak season volumes will be comparatively mild. Transpacific contracts appear to have settled in the $1,200-1,400 range to the US West Coast, although a large number of NVOCC contracts are yet to be finalised.

ONE and COSCO’s financial results released last week confirmed that carriers were still profitable despite the sharp fall in 1st quarter earnings, which explains the lack of capacity discipline exhibited by the carriers so far.

Johnson Leung

Johnson Leung

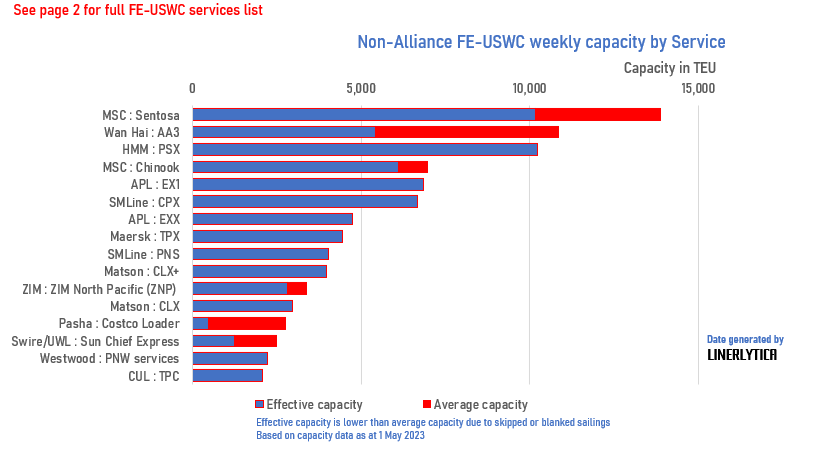

The number of Asia-US West Coast services that are operated independently outside of Alliance arrangements has shrunk from over 40 in 2021-22 to just 16 currently following the withdrawal of the smaller carriers such as Transfar, BAL, CIMC, TS Lines and SeaLead while MSC, Zim and Wan Hai have also cut the number of independent services that they operate. Overall capacity on the FE-USWC route is down 15.6% based on the current 13-week average compared to the same period last year.

See page 2 of full report for full FE-USWC services list (subscription required).

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year