No sooner had the transpacific rates rebounded than the carriers started to cut rates again, in a pattern that will likely be repeated over the coming months. The SCFI spot rates to the US West Coast slipped 2% last week after rising by 29% a week earlier. Another attempt to raise freight rates will be made in mid-May, with carriers already deferring the 1 Mayaa GRI due to the Labour Day holidays as cargo volumes are unable to support rate hikes despite the blanked sailings planned in early May to coincide with the week long holidays in China. Maersk still has the largest number of idled ships while its main rivals remain adamant in chasing market share.

A large number of transpacific contracts have yet to be concluded, with negotiations with NVOCCs particularly problematic for carriers given the current rate volatility. Some carriers have extended preferential NVOCC rates to the end of June as the share of contract volumes have shrunk to less than 30%.

Johnson Leung

Johnson Leung

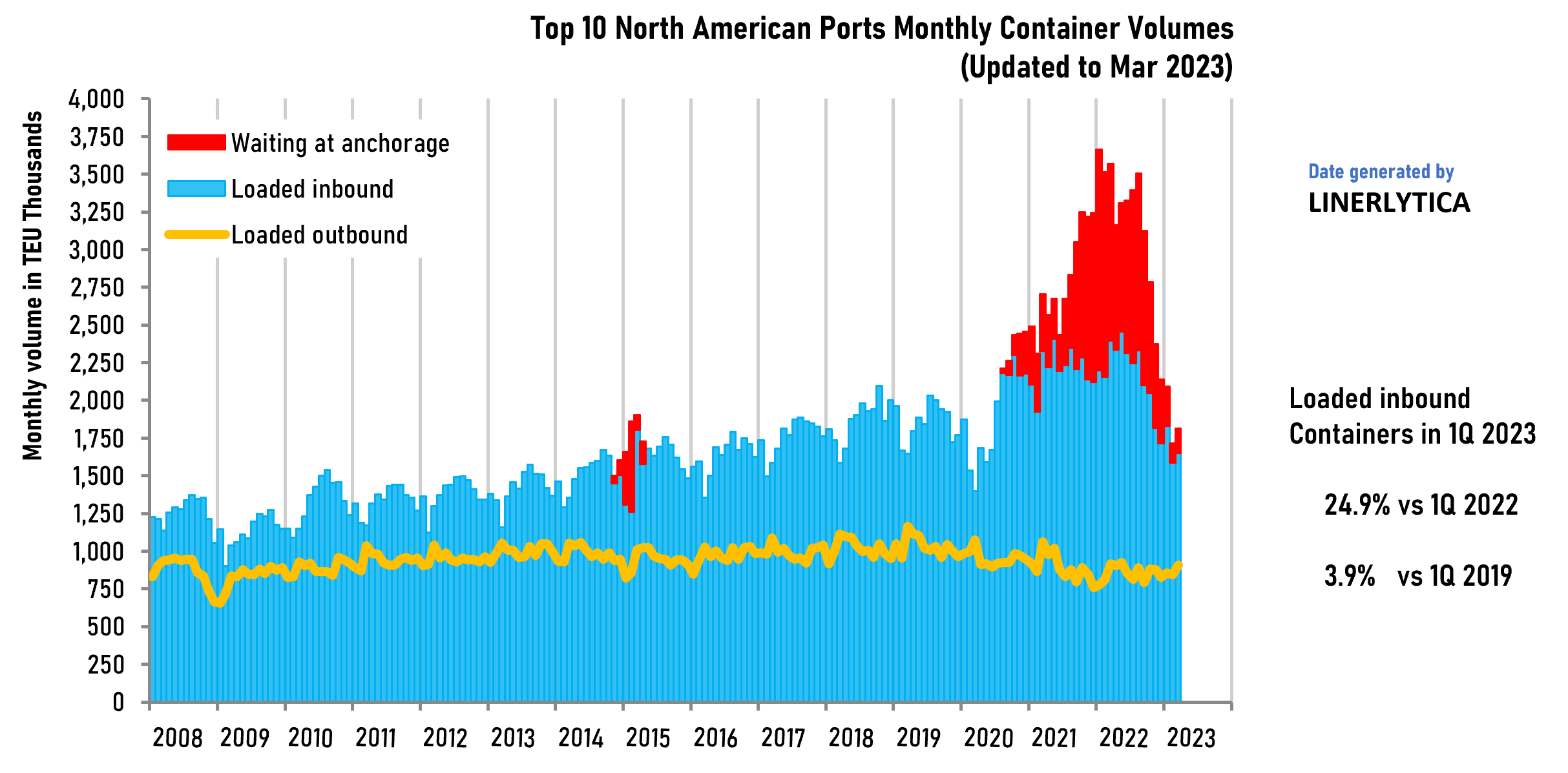

Transpacific container volumes have fallen sharply in the first quarter of 2023 as reflected in container volumes at the 10 largest ports in North America. Total laden inbound containers handled at the 10 ports dropped by 24.9% in the first 3 months of 2023 compared to the same period in 2022. The 1Q volumes are even lower than pre-pandemic volumes, as it is 3.9% below the corresponding period in 2019. Port congestion has also declined sharply, with the total containership capacity waiting at North American ports falling from 1.17m teu at the end of March 2022 compared to just 0.16m teu in March 2023.

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year