Freight rates have rebounded strongly on the back of the mid-April GRI, with the SCFI up 8% last week due mainly to rate increases on the Transpacific, Middle East and Latin America routes. Transpacific spot rates increased by 29% to the US West Coast to over $1,600/feu, providing carriers some leeway to negotiate contract rates at $1,400-1,500/feu – a level that would not be possible to achieve if spot rates had remained in the $1,000-1,200 /feu level before the rate increase. Carriers’ discipline will be tested in the coming weeks to see if the higher rates would hold, and if the carriers can push through the next round of GRI scheduled for 15 May.

Capacity utilisation has dropped this week, with more capacity returning to the market even as new ship deliveries continue apace. Idled capacity has dropped to its lowest levels since November and currently stands a just 1% of the total fleet compared to its recent peak at 2.5% in February.

Johnson Leung

Johnson Leung

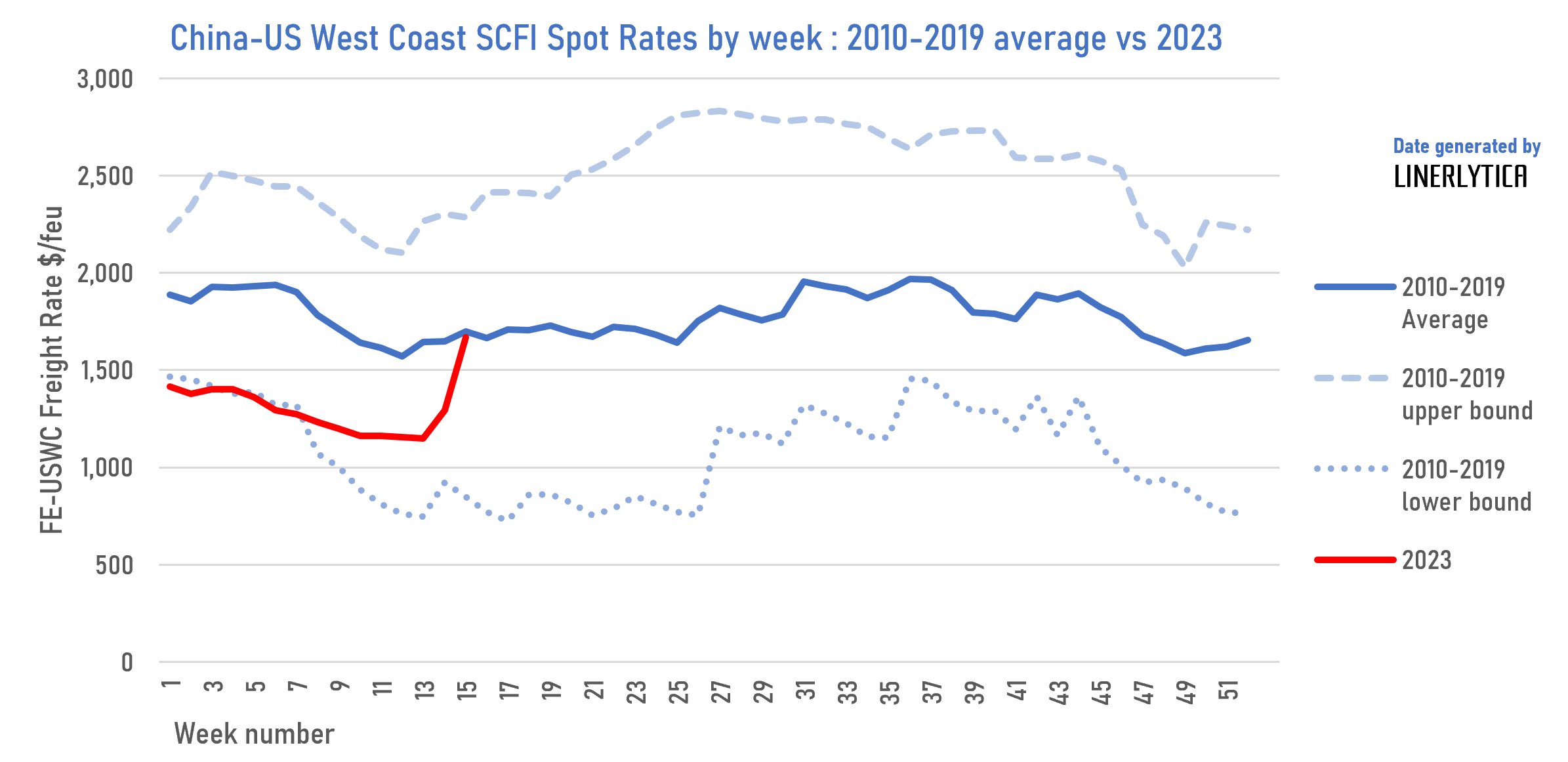

The transpacific trade will see more rate volatility this year, with the mid-April GRI only the first of multiple attempts by carriers to push through higher rates after the catastrophic drop since late last year. Spot freight rates to the US West Coast are well below the pre-COVID average (based on the 2010-2019 SCFI weekly data) and are near the bottom of the rate range of the last decade. Spot rates were exceptionally volatile in the 2012-2016 period with carriers imposing rate increases practically on a monthly basis but failed to prevent rates from slipping. A similar rate pattern could be repeated this year, especially if cargo demand remain weak over the summer peak season.

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year