Market sentiment turned positive for the first time since September 2022, with rising conviction around a mid-April rate increase on some key routes. Carriers are making a last-ditch effort to raise spot rates on the Transpacific ahead of the 1st May contract season with rates expected to rise by $500-600/feu.

The SCFI rebounded marginally last week on improved rates in the Middle East and Latin America on the back of stronger demand but further rate increases in April will provide carriers with much needed relief after spot rates dropped by over 80% since last year. Carriers’ resolve to maintain pricing discipline will continue to be tested in the coming months as charter rates and resale prices continue to rise, with vessel availability declining rapidly and carriers are showing renewed confidence to push ahead with new capacity additions as the summer peak season approaches. New ship deliveries reached a 5 year high of 200,267 teu last month and is on track to exceed 2.2m teu in 2023.

Johnson Leung

Johnson Leung

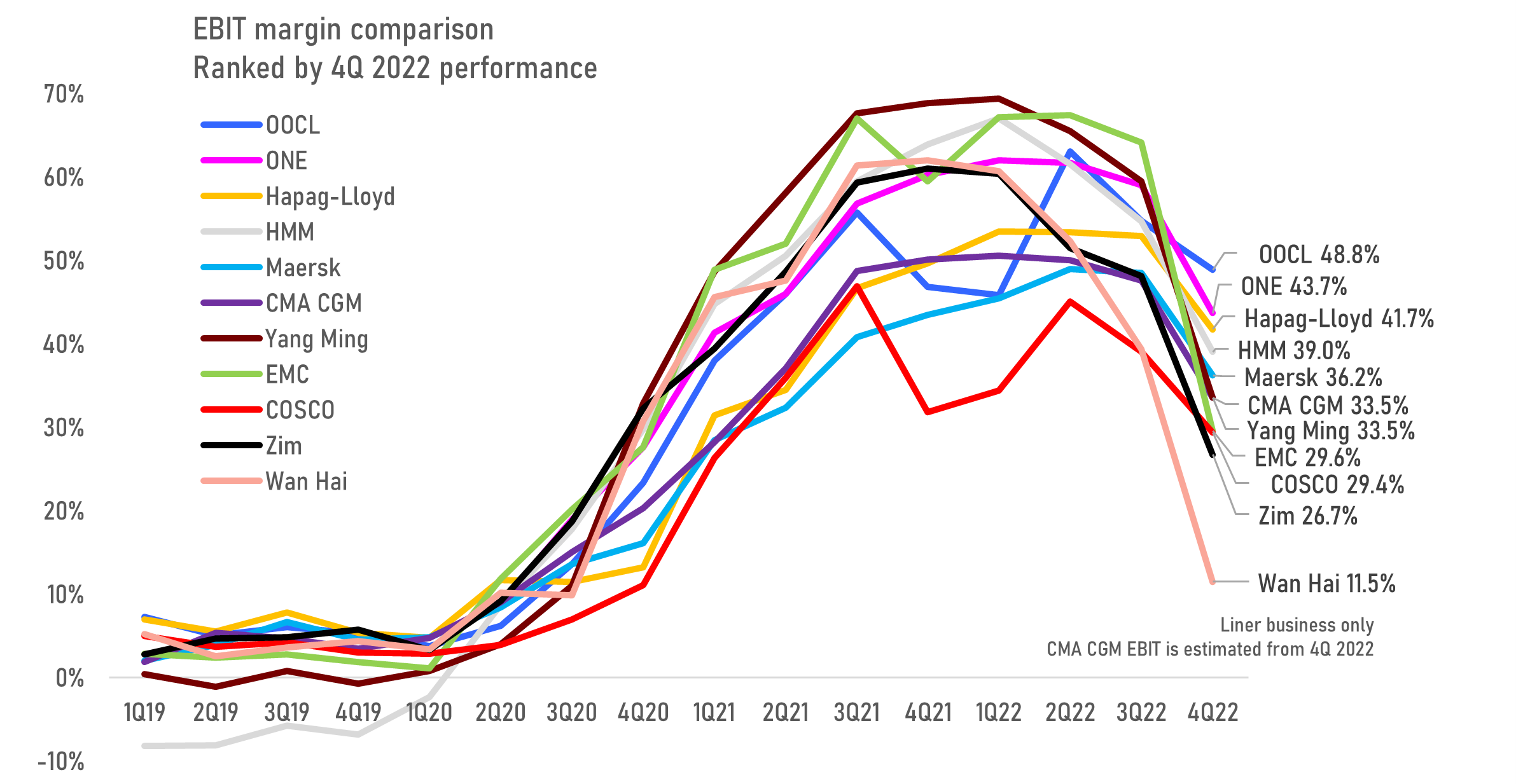

Carriers recorded mixed results in the last quarter of 2022, with average EBIT margins falling from 50.5% in the 3rd quarter to 35.7% in the 4th quarter. Amongst the main carriers, OOCL topped the carrier earnings table, aided by its stable trade mix and presence on the Trans-Atlantic trade where earnings outperformed the Asia-export based trades. Carriers with a higher exposure to the volatile spot market and lower contract volumes recorded the sharpest drop in earnings, with Wan Hai and Zim being particularly vulnerable to the correction in spot freight rates.

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year