Market sentiment has turned positive for the first time since August, with momentum building for the November freight rate hikes as further capacity cuts are forthcoming after THE Alliance decided belatedly to suspend the EC4 service to the US East Coast via the Suez in November. This follows earlier cuts made by various carriers on the USWC and Europe routes that have helped to elevate carriers rate restoration efforts. The SCFI recorded its 2nd successive weekly increase, led by gains on the Middle East, Latin America and Australia routes while Asia-Europe and Transpacific rates are largely holding ahead of the planned rate hikes in November.

Despite the more bullish sentiment, carriers’ ability to hold on to the rate increases will be tested in the coming weeks as the premature re-introduction of withdrawn capacity will risk unravelling the initial gains with unrelenting pressure from the new vessel supply pipeline.

Johnson Leung

Johnson Leung

Idle fleet needs to rise further for rate hikes to stick

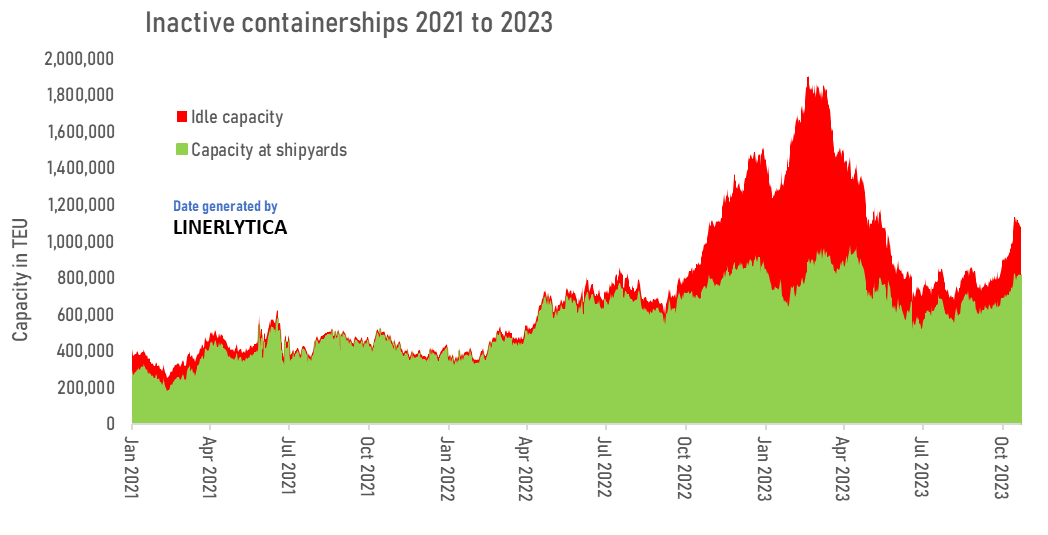

The current idle fleet remains too low to sustain the rate hikes planned in November with at least 1m teu of excess capacity that needs to be removed over the next 2 months in order for the rates to stick. The task will be made more difficult by the over 500,000 teu of new deliveries scheduled to be delivered before the end of the year, which will require more ships to be idled upon delivery. The recent rise of ships in drydock has helped to remove some of the excess capacity but it also means that more refurbished ships will be returning to the market next year even as scrapping rates remain stubbornly low.

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year