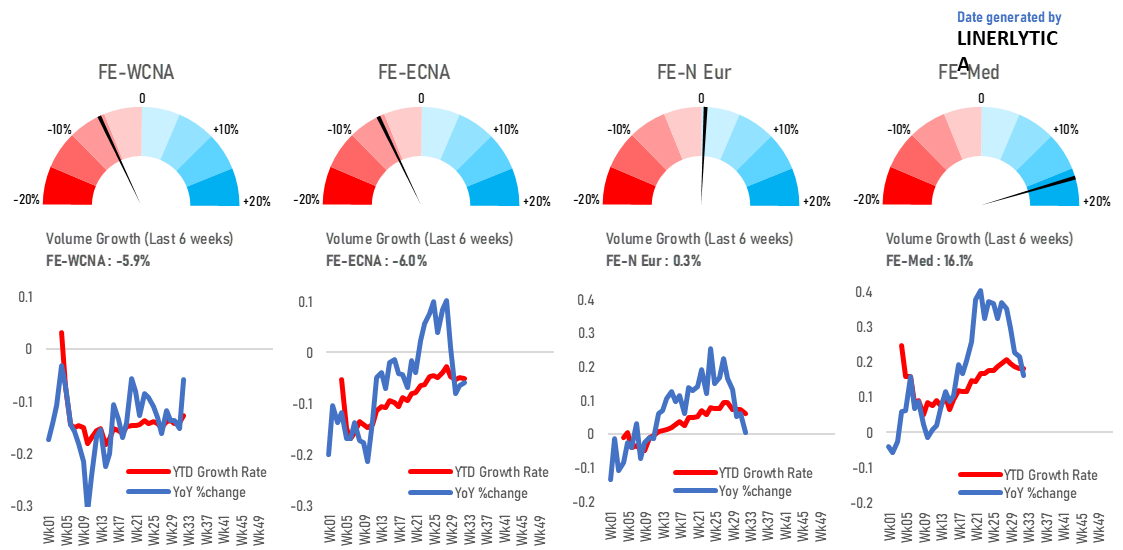

The SCFI extended its gains for the 3rd consecutive weak but there are signs that peak season volumes are already starting to fade and the recent rate rebound could soon run out of steam. Transpacific freight rates have led the recent gains on the back of rising demand and capacity cutbacks, with Asia-Europe rates also managing to retain most of their recent gains despite more shaky market conditions. However, Linerlytica’s trade volume indices have slipped over the last 4 weeks on 3 of the 4 key trades (FE-ECNA, FE-N. Eur and FE-Med) with only FE-WCNA holding steady but on a weaker base against last year’s volumes.

Despite widely reported congestion at the Panama Canal, the restrictions have no material impact for the container sector, with priority passage given for regularly scheduled services and no significant delays reported apart from irregular loaders which can be diverted to the Suez route.

Johnson Leung

Johnson Leung

Peak season volumes beginning to fade

Linerlytica’s trade volume indices have started to weaken over the last 4 weeks after peaking in July. Volume growth has been rising steadily over the 2nd quarter but the positive trend has reversed on 3 of the 4 main trade routes (FE-ECNA, FE-N. Eur, FE-Med). Volumes on the FE-WCNA route are still holding but growth rates on this route have been negative throughout this year, with support for the recent rate rebound coming solely from capacity cuts. Total capacity on the FE-WCNA route is down by 6.8% yoy, compared to rising capacity deployed on the FE-ECNA (up 3.4%), FE-North Europe (up 7.7%) and FE-Med (up 26.1%).

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year