The resolution of the ILWU US and ILWU Canada port labour contract negotiations have removed the last hurdle to market normalisation, with port congestion set to ease further from its current level affecting 5.7% of the global fleet.

This does not bode well for the container market that is increasingly struggling with surplus capacity. Zim downgraded its EBIT forecast last week to a full year loss of up to $500m from its earlier prediction of a $100m-500m gain, with carriers abandoning the narrative of a 2nd half market recovery.

The transpacific is however bucking the negative trend, as it single handedly lifted the SCFI by 5.1% last week, with the US West Coast rates soaring by 26% to reach a 9 month high. Momentum is strong for another transpacific rate hike on 1 August, aided by capacity cuts and peak season demand, with disruptions from the 2-week port closure on the Canadian pacific coast also helping to the keep capacity utilisation sufficiently high for the rate increases to stick.

Johnson Leung

Johnson Leung

A Tale of 2 Trades

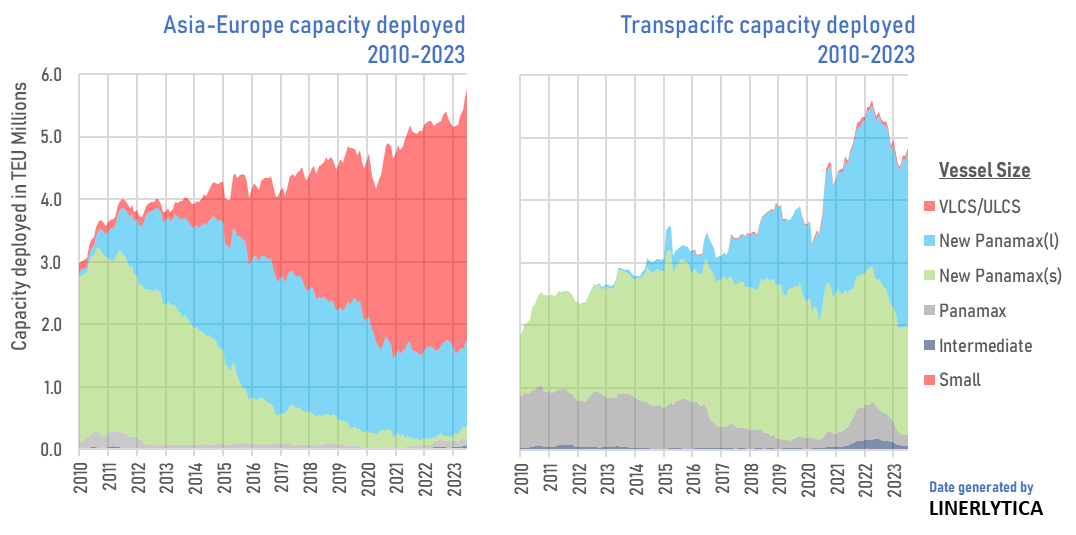

Transpacific freight rates have enjoyed a minor revival after 2 successive rate increases in July, with a fresh round of rate hikes planned in August. In contrast the Asia-Europe rates are still falling, dragged down by the incessant capacity pressure from the delivery of new 24,000 teu ships. Total capacity deployed on the Asia-Europe route is up 7.6% yoy, compared to a 12.1% decline on the Transpacific route, with further divergence expected in the coming months as even more capacity is added to Europe while capacity are being withdrawn from the Transpacific market.

Weekly/Monthly Market Pulse: US$1,500/US$1,800 per year