MARKET BRIEF – 2022 WEEK 10

Spot freight rates dropped for the 9th consecutive week, with further falls expected in the next 2 weeks as carriers were unable to push through with mid-March rate increases amidst soft volumes across all main tradelanes. The weakness has not deterred carriers from chasing tonnage as charter rates and resale prices continued to rise, and fresh ship orders have been unveiled in the past week that brought the containership orderbook to a new 10-year high of 25.3%.

Global port congestion is easing slightly, with improvements in North America partly offset by deteriorating conditions in North Europe. Chinese port congestion remains low for now, but China has imposed stricter COVID measures that could affect cargo flows especially in South China

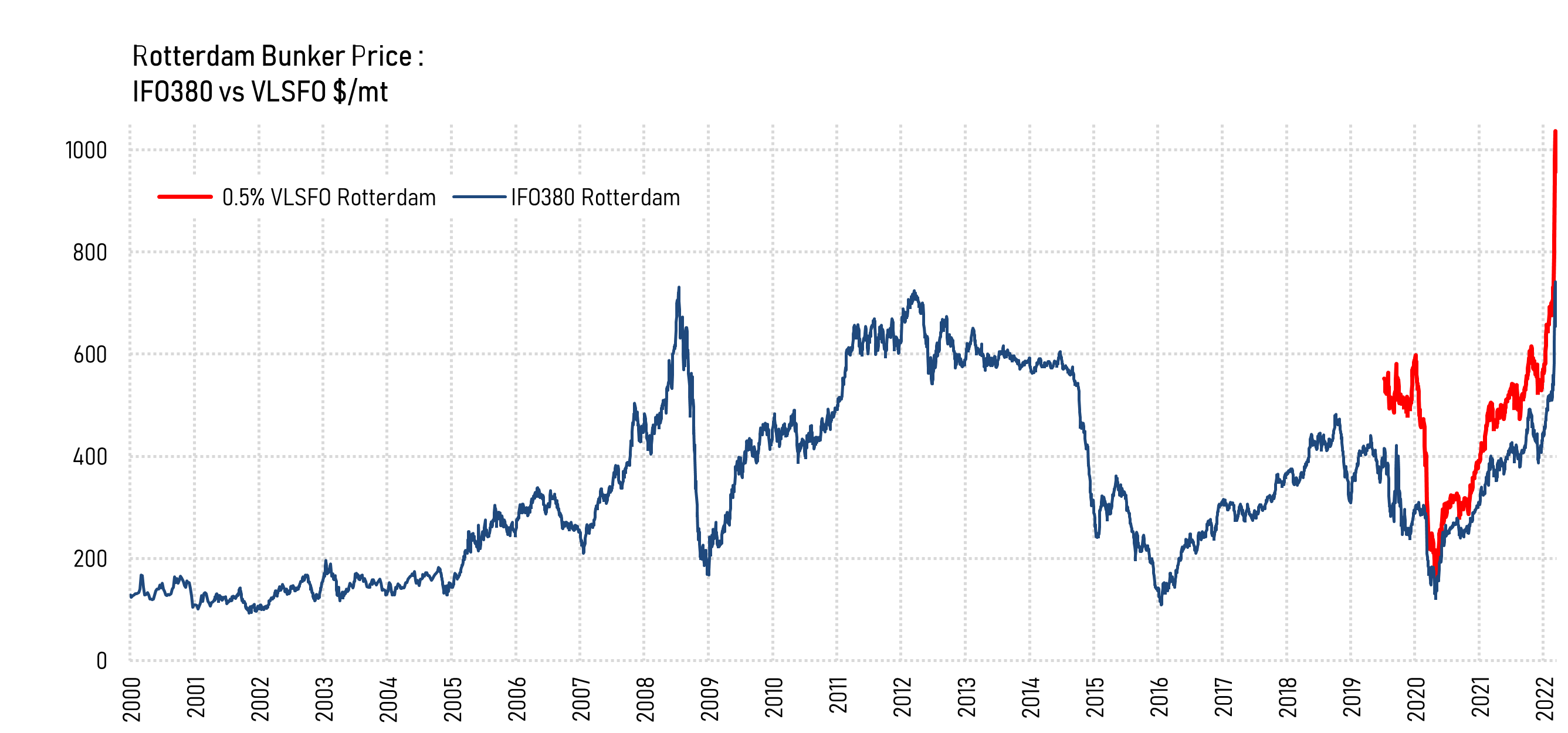

Bunker fuel prices surged to a record high last week but closed 12% below the peak in volatile trading in the most direct impact of the Ukraine crisis on the container shipping market so far. Average VLSFO prices last week was 24% higher in Rotterdam at $978/mt, while the VLSFO-HSFO price spread reached $274/ton, matching the record high in early 2020 when the initial demand surge for VLSFO increased the price spread. The higher spread will benefit carriers that have invested heavily in SOx exhaust scrubber systems, with HMM (83%), Evergreen (75%) and MSC (46%) the main beneficiaries – see page 2 for full fleet breakdown by fuel type for the main carriers

Discount offer at $1,200 p.a. before end of March